South Africa

South Africa Namibia

Namibia

Bernard Fick

Chief Executive

Letter from the CEO - Q1 2020

Article Summary

This article is from the Quarter 1 2020 edition of Consider this. Click here to download the complete edition.

Welcome to the first edition of our digital-only version of “Consider This” for the first quarter of 2020. We trust that you will enjoy this greener, more sustainable and more flexible platform that we can tailor to better meet your interests. Rest assured that we remain committed to providing the same high-quality articles offering our investment views, investor education and personal finance insights that the printed version offered.

Global equities end 2019 with good gains

Turning firstly to 2019 market developments: after a tough three quarters of 2019, the final quarter of the year proved to be more positive for South African investors thanks to some progress made in the US-China trade war and some finality being reached around the Brexit saga. The Conservative party’s decisive win in the December United Kingdom general election provided a clear mandate to that government to conclude the UK’s exit from the European Union by 31 January 2020, notwithstanding the disruption this will cause.

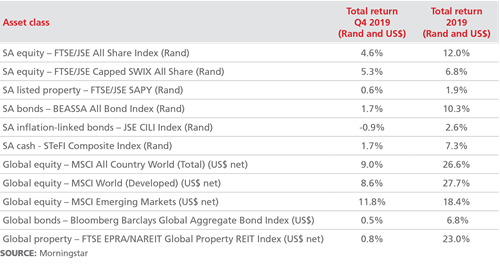

These developments propelled global equities to their strongest annual returns in a decade, with the MSCI All Country World Index returning 26.6% in US dollars for the year, as shown in the table. Emerging market equities and currencies were also boosted by the renewed bullish sentiment. Equally, global bonds delivered a surprisingly strong 6.8% total return for the year, considering the high prices at which they started. This environment provided support to the performance of the Prudential Global Funds range, into which the offshore portions of our South African client portfolios are invested.

SA benefits from bullish sentiment

South African equities and the rand were also beneficiaries of the more positive global mood, helping to offset negative local developments during Q4. However, the resumption of load-shedding was a significant setback to our hopes for increased economic growth.

The FTSE/JSE All Share Index produced a 13.3% return for the quarter and 12.0% over 2019 on a total return basis, while the FTSE/JSE Capped SWIX Index (which caps single shares to a maximum index weight of 10%) delivered 5.3% and 6.8%, respectively.

This substantial differential, and our reasons for preferring the Capped SWIX benchmark in managing our funds, are explained in an accompanying article by our Head of Quantitative Analysis, Clare Lindeque.

Despite local corporate earnings broadly surprising to the upside, our market did not experience a similar re-rating to that in most other global equity markets, including our emerging market peers. Foreign (and local) investors remain rightly concerned about South Africa’s slow economic growth, government finances, Eskom and further credit rating downgrades going forward.

Listed property recorded another poor year, producing 1.2% for Q4 and -0.4% for 2019. South African bonds delivered a 1.7% return in Q4 and a commendable 10.3% for the year. The gains were driven largely by falling inflation throughout the year − November CPI reached a nine-year low at 3.6% year-on-year. South African bonds’ high real yields relative to most other countries did attract buying from yield-seeking investors. Cash (as measured by the STeFI Composite) delivered 1.7% and 7.3%, respectively. Finally, the rand gained ground in Q4 against all three major global currencies, along with other emerging markets, and for the year it appreciated 2.7% versus the US dollar and 4.5% against the euro, but lost 0.5% against the pound sterling.

Prudential wins Raging Bull award

Looking at our fund performance, first of all I’m pleased to report that the Prudential Global Inflation Plus Feeder Fund has won a Raging Bull Certificate for its risk-adjusted performance over five years to 31 December 2019 as the “Best (SA-domiciled) global multi-asset low equity fund”.

The fund is a rand-denominated fund investing (or feeding) directly into our Prudential Global Inflation Plus Fund, part of the Prudential Global Funds range of four offshore Irish-domiciled US-dollar global funds. The range is managed by our largest shareholder, London-based M&G Investments. The award is testimony to the long experience and skills of the large investment team at M&G Investments, as well as the benefits of having a fund range designed specifically for South African investors.

Prudential fund performance

On a more general note, while the absolute investment returns from our funds did improve from 2018, 2019 was still a fairly disappointing year in terms of fund performance. Absolute fund returns reflected the weak economic conditions prevalent in South Africa while, somewhat counter-intuitively, rand appreciation detracted from the stronger returns of our offshore holdings.

Our relative fund performances, when compared to their benchmarks, were also disappointing over the 2019 calendar year, following on a very strong set of relative returns in 2018.

On the positive side, our funds benefitted from our overweight positioning in global equities and underweight in global fixed income, plus select holdings in large international rand-hedge shares such as British American Tobacco, Anglo American, Richemont and Naspers. However, detracting from value, when compared to our benchmarks, were our overweight positions in Sappi and Sasol and underweight positions in precious metals producers like Sibanye Gold, Implats, Amplats and Northam.

While it is always easier to discuss our positions that added value, some investment ideas did cause portfolio underperformance. When this happens, our approach is to carefully reconsider our investment case, to determine: (a) whether we made a mistake in our analysis; or (b) whether our analysis remains defendable. If it is the former, we should reduce or close our positions. But when it is the latter, we should hold our positions or even add thereto, even though that is emotionally a very tough thing to do. Below are very brief summaries of our two largest single stock detractors over the year, and our arguments for still holding these positions in our client funds:

Sappi

Sappi Limited, the South African-based paper company, was one of the top contributors to performance for the final quarter of 2019, but the largest detractor from performance for the full year over most of our client portfolios. We have held Sappi for several years based on an investment case premised on the company paying down its large debt balance and having considerably lowered the cost of this debt which it accumulated during the financial crisis. We recognised that Sappi was aggressively allocating capital away from its declining paper business and investing heavily in its dissolving pulp business. (Dissolving pulp is the product mainly used in the production of clothing and has been growing quickly as a cheaper alternative to cotton.) Until 2019, this investment case had played out well, as Sappi has paid off and refinanced debt to much lower levels of interest and is now making well over half its profits from dissolving pulp. Most importantly, Sappi has resumed paying dividends and this had underpinned its share price recovery.

Unfortunately though, the price of dissolving pulp dropped significantly in 2019 (with a rebound in the final quarter), and the market penalized the Sappi share price as result. In our analysis, this market reaction was overdone. Our investment case remains intact, only somewhat delayed. While we remain cognisant of the risks that Sappi faces with respect to falling paper demand and the global trade conflict, the company is a major global supplier of cellulose pulp, and generates very good margins from this business, in spite of the lower prices now being achieved. Sappi also continues to generate strong cash flows. On a valuation basis, Sappi is near the most attractive levels we have seen in last decade. At the same time, it is also in a far better financial position than it has been in the last 10 years and paying sustainable dividends.

Sasol

Our overweight position in Sasol was a detractor to fund returns over 2019, both in absolute and relative terms. Its share price rallied in the latter part of the fourth quarter of 2019, with the successful replacement of the reactor catalyst at the ethane cracker of the Lake Charles chemicals project (LCCP), but this did not offset losses earlier in the year, when the company surprised the market with a huge US$1.1 billion spending overrun for the project. The LCCP has been a continual disappointment for the company and us as shareholders as it has run significantly over budget and behind schedule. And now that the project is finally on-stream, Sasol is ramping up production into a weaker chemicals market than when the project commenced. The poor execution of this project has cost shareholders a significant amount, and led to the departure of a number of very senior Sasol executives.

Our investment case is based on:

- Solid earnings from the company’s existing operations (although with a weaker balance sheet) that support earnings per share; and

- Improving cash flow after the completion of the LCCP project beginning to contribute positively to earnings. Although the higher-than-expected debt (which will now take longer to pay off) and the slower ramp-up to “steady-state” earnings does dampen the benefit compared to our prior expectations, cash flow is not expected to be impacted as much because the group will postpone additional planned capital investment for other projects to compensate for the extra US$1.1bn Lake Charles expenditure.

More positively, Sasol was able to increase its debt covenants and the strength of the oil markets in the fourth quarter of 2019 has lowered the risk of a capital call from shareholders.

We still expect a significant “cashflow inflection point” for the company in 2020/21, when positive operating profit from LCCP replaces significant capital spending to build the plant. The cash flows that the project will generate should be able to adequately pay down debt. However, the risk of dividends being cut has increased. In fact, it might be the best course of action for Sasol to temporarily suspend dividends in order to further pay off debt and rebuild its balance sheet.

In our view, a share price correction was warranted following the LCCP challenges, but it has been overdone. Sasol’s capital allocation plan commits the company to further reducing its debt through asset sales, as well as curtailing its further capex spending. As such, its balance sheet strength is set to improve further along with free cash flow. Our current assessment is therefore that our Sasol investment case still holds, but we acknowledge it has become slightly less convincing.

Asset Allocation Decisions Added Value in 2019

Across our multi-asset Balanced and Inflation Plus Funds we continued to hold a meaningful exposure to domestic and global equities, especially as the former’s valuation became cheaper over the year. In fact, over 2019 we added to our SA equity exposure as valuations fell. Despite their underperformance, we remain convinced that over the longer term, equities will deliver superior real returns.

We remained underweight in listed property for the year given the higher risks to earnings going forward despite the apparently attractive valuations prevailing. The sector faces ongoing headwinds arising from pressure on landlords to reduce their rentals, due to both weak consumer spending and office oversupply. In retrospect, we should have been even further underweight.

Also adding to performance across most of our multi-asset portfolios in 2019 was our overweight holding in South African nominal bonds, which offered an attractive real return of over 5.0%. However, we did miss out on some additional return through our preference for longer-dated bonds beyond 10-years, which did not perform as well as their shorter-dated counterparts.

Looking to 2020

It is disappointing that nearly two years after “Ramaphoria” little progress has been made on structural reforms or state-owned enterprises (SOEs) finances – and Eskom blackouts have returned to further weigh on growth. Not surprisingly, consumer and business confidence remain depressed and we suspect the consumer will remain under pressure in 2020. Consequently, we don’t deny that South African risks remain high, and growth expectations subdued. Notwithstanding this, our financial markets look to price the future, and with most local asset class valuations looking very cheap - in particular, equity valuations approaching all-time lows - perhaps even modest indications of progress could produce reasonably good returns for investors.

As long-term valuation-based investors, we have been using this opportunity to add cheap holdings in quality companies to our client portfolios. This should bode well for future returns over the medium term. Sandile Malinga, portfolio manager, discusses our return outlook in more detail in our Table Talk feature in this edition.

In these challenging times, we promise to remain patient, keep a long-term outlook and follow our consistent investment process to deliver competitive, inflation-beating returns for all our clients.

We hope you enjoy this Q1 2020 edition of Consider this, and as always welcome any feedback you may have.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter