South Africa

South Africa Namibia

Namibia

Clare Lindeque

Head of Quantitative Analysis

SA equity returns in 2019: Decent or a disappointment?

This article is from the Quarter 1 2020 edition of Consider this. Click here to download the complete edition.

Clare Lindeque, Head of Quantitative Analysis, explains why investors need to understand which equity index is used in managing their portfolios, both to avoid confusion over returns and to ensure they have the most appropriate measure to meet their own investment goals.

Key take-aways

- It’s very important that investors understand which equity index is used in managing their portfolios, to avoid confusion over returns and to ensure they have the most appropriate measure to meet their own investment goals.

- There are four broad SA equity indices commonly used, and each has their own merits. Each also outperforms depending on market conditions, none regularly outperforming another.

- Prudential, along with many other investment managers, uses the Capped SWIX Index in managing most of our unit trusts due to it being the most accurate representation of the SA equity universe available to investors, its lower risk characteristics, and its ability to deliver returns comparable to the other broad SA market indices.

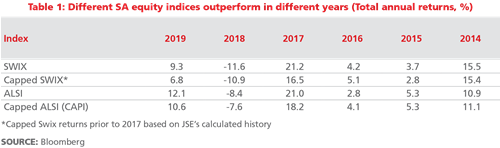

Either South African equities returned 12.1% in 2019, a decent result in line with the long-term average, or they delivered 6.8%, certainly disappointing when compared with their history. Which is correct? As an investor, it can be perplexing when the numbers differ so much. Anyone hearing that the FTSE/JSE All Share Index (ALSI) returned 12.1% – the most widely used measure in news reports – would be disappointed to learn that it was actually the 6.8% from the FTSE/JSE Capped SWIX Index (a very common index used by investment managers) that was most applicable for their portfolio’s equity performance.

In truth, as Table 1 shows, both results are valid, and in fact there are several correct return measures for our equity market for 2019. South Africa has four different broad indices that measure equity performance, and it’s important to know which of the four is most relevant to your portfolio. All four have outperformed in recent years, depending on market conditions. Here we take a closer look at the South African equity market indices, and why their performance diverged so much in 2019.

Which SA market indices are available?

In the FTSE/JSE suite of broad market South African equity indices, the headline index is the All Share Index (ALSI), which has been in existence – in one form or another – for decades. The Shareholder Weighted All Share Index (SWIX) was introduced in 2002. The share universe for these two indices is identical, comprising 99% of the full market capitalisation of equities listed on the JSE’s main board. Market capitalisation (or market cap) is the value of a company, determined by the number of its shares in issue multiplied by its share price. An index’s value or market cap is therefore the sum of all the individual companies included in the index. Currently this universe comprises 158 companies.

The ALSI and SWIX differ in how their constituents are weighted. Both are weighted by their market cap and their free float; the larger a company’s market cap, the larger its index weight, before any other adjustments are applied.

There are also liquidity and free float requirements for index inclusion. Liquidity refers to the ease of trading of a share, which can be impacted by its scarcity and how often it trades. Meanwhile, free float is the portion of a company’s common stock that is freely tradeable. Any equity tied up in strategic ownership by other companies, owned by employees, or whose sale is subject to lock-in clauses, for example, is excluded from a company’s free float. Both the ALSI and the SWIX index weights are adjusted for free float, but some of the ALSI weights have a quirk related to this.

Here’s the quirk. Since 2013, all foreign stocks that have sought an additional listing on the JSE have had their ALSI and SWIX weights calculated based on a SWIX free float factor. This is a weighting scheme where only the portion of each company’s freely traded share capital that is held on the South African shareholders’ register is counted towards the share weight – hence the origin of “shareholder weighted” index. However, those stocks with foreign listings on the JSE prior to 2013 were able to retain their previous ALSI weights based on their full market cap, and are not subject to SWIX free float.

Consequently, these “grandfathered” companies, for whom the shares held by South African investors may represent only a small portion of their total shares outstanding, have higher weights in the ALSI than in the SWIX. Examples include BHP Group, Richemont, Investec plc and Anglo American. This has also contributed to the higher weighting of the Basic Materials sector in the ALSI (30.8%) than the SWIX (20.2%). In 2019, this was one of the drivers of the outperformance of the ALSI over the SWIX, as we explain later.

Index concentration and capped indices

A significant shortcoming of market cap indices, but one that reveals itself only a few times in a generation, is the fact that this weighting scheme can lead to a massive concentration of index weight – and single stock risk – in companies or sectors that grow at an outsize rate in comparison to their peers. When an index has a large portion of its weight in a small number of stocks or certain sectors, it is referred to as a concentrated index.

Notably, South Africa’s equity market is among the most concentrated in the world. It’s well known that in the past the dominance of the resources sector (and Anglo American and BHP in particular) during peak commodity cycles presented undue risk to local investors. This particular over-representation has now waned in line with global commodity prices. More recently, Naspers has been the heavyweight stock of most concern to investment managers, having peaked at 26.9% in the SWIX in early April 2019. This was before its separate listing of Prosus in Amsterdam, which has brought its weight down to 17.7% in the SWIX as of the end of 2019.

The implications of index concentration are potentially serious; companies that grow at a wildly disproportionate rate in comparison to their peers rarely maintain this colossal size. Furthermore, investors in market indices – or in tracker or passive funds benchmarked to market indices – dominated by few stocks are exposed to a large amount of specific risk. This is risk that is particular to each company, or to a sector; it is also the kind of risk that you can diversify away by holding a well-balanced portfolio. You’d advise your grandma against investing all her savings in one stock; the case of investing in a highly concentrated index is analogous.

To mitigate against single-stock risk, the JSE introduced two capped indices: the Capped All Share (CAPI) in 2003 and the Capped Shareholder Weighted Index (Capped SWIX) in 2016. These indices comprise the same universe of companies as the ALSI and SWIX, but the maximum individual stock weight is capped at 10%. The weights of other stocks in the index are slightly increased as a result. The CAPI follows the ALSI weighting scheme, and the Capped SWIX follows the SWIX.

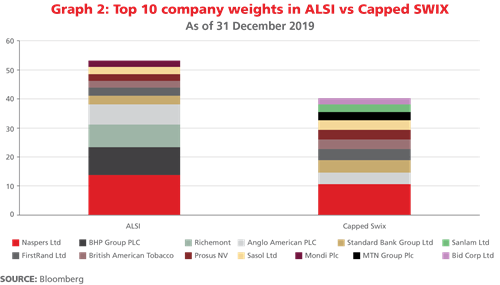

Because the SWIX and capping methodologies limit the weighting of offshore and larger companies in their indices, there ends up being some significant differences in composition between the headline ALSI, which most people commonly refer to when following the market, and the Capped SWIX. Graph 2 compares the top 10 shares by weight in each index. It highlights two of the most notable differences, which are the underweighting of large global companies in the Capped SWIX, and the higher concentration risk in the ALSI.

Index performance in 2019

It is impossible to predict whether one benchmark index will outperform another in a given year. In fact, if we had that kind of foresight, we’d be using it in other ways! As you can see from Table 1, there isn’t any one particular index that systematically outperforms the others; capped SWIX was the top performing of the four FTSE/JSE indices in 2016. Depending on how market prices move, the characteristics of different index construction methods manifest themselves.

It is, however, possible to explain relative index performance after the fact. Taking a broad view of 2019’s return differential between the ALSI and the Capped SWIX , the underperformance of the Capped SWIX was attributable to its smaller exposure to the large global stocks, many of which performed strongly in 2019. More specifically, the three primary reasons were due to differences in index weighting in 1) the Basic Materials sector, 2) Naspers and 3) Richemont.

First, the best-performing sector in the SA market for 2019 was Basic Materials, which includes gold, platinum, and diversified mining companies. Some of these stocks – particularly the gold and precious metal (platinum, rhodium, palladium) miners – generated returns in excess of 100% for the year. These returns were driven by surging palladium and rhodium prices, underpinned by increased demand, and a rallying gold price thanks to its safe-haven status on the back of elevated geopolitical risk.

The ALSI has a higher weight in dual-listed resource counters than the SWIX (and thus than the Capped SWIX, too). For example, the ALSI’s weight in BHP was 9.6% at the end of December 2019, whereas its Capped SWIX weight was only 2.1%. Overall, Basic Materials contributed 7.3% of the ALSI’s 12.1% total return for the year, and 5.3% of the Capped SWIX’s 6.8% annual total return.

The second most significant contributor was their weights in Naspers, which represented 13.8% of the ALSI and was constrained to only around 10% of the Capped SWIX. Naspers delivered a 19.9% total return for 2019, thus contributing 3.8% to the ALSI total return, and only 1.9% to the Capped SWIX total return.

The final major difference was their respective weights in Richemont, one of the grandfathered companies, that had a weight of 7.8% in the ALSI and 1.8% in Capped SWIX at the end of 2019. Richemont returned 20.1% for the year; as a result it contributed 1.4% of the ALSI’s 12.1% total return, and only 0.3% to Capped Swix.

Interestingly, for both indices, the remainder of the shares in the market (excluding Basic Materials, Naspers and Richemont) produced a negative total return in aggregate.

Choosing our equity index

At Prudential, for our institutional or segregated clients, we manage their portfolios using the indices that they request - those that are best aligned to their unique requirements.

Where we have full discretion as to which index to choose for our clients, such as in our retail unit trusts, we use the Capped SWIX Index. This holds true across all of our equity and multi-asset portfolios where our aim is both to protect and grow our clients’ longer-term retirement savings. That protection involves limiting potential negative returns from event-specific risks, like a market crash, as well as SA-specific risks, such as those related to certain companies, sectors or unique market conditions.

In analysing our market indices, we know that the SWIX best represents the share universe available to a South African investor. For example, all South African managers could not hold a 7.8% position in a dual-listed company like Richemont (its ALSI weight), as this weight includes shares listed in Switzerland, which a 100% locally restricted fund could not access.

Equally, we prefer Capped SWIX to SWIX because it somewhat reduces the very high concentration risk in our market by setting the maximum index weight to 10%. By incorporating the Capped SWIX into our investment process, we are implicitly limiting portfolio downside. Additionally, our investment process features explicit maximum limits for portfolio weightings of 5% for each sector, and 4% for an individual stock, as further layers of protection.

Know your index

In conclusion, we believe it’s very important for investors to understand which SA equity index is most suited to their own investment goals and risk appetite. Be aware of the risks involved, like market concentration risk. For those preferring to have their investment manager choose for them, then they should know which index they use and why. This is especially true in passive investing, where the fund tries to replicate the index exactly.

For Prudential’s South African equity portfolios, our preference for Capped SWIX is based on its appealing combination of improved risk characteristics over the more concentrated indices, and its ability to deliver returns comparable to the other broad SA market indices. It’s a choice we are confident will keep delivering strong returns for our clients over the years.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter