South Africa

South Africa Namibia

Namibia

David Knee

Chief Investment Officer

Market Observations: Q1 2023

So far in 2023, global financial markets have experienced wild swings – particularly in the normally less volatile fixed income markets – dictated by the guessing game over the path of US interest rates, inflation and growth. January’s sentiment was relatively bullish, dominated by expectations of a weaker US economy going into 2023, which would have increased the likelihood of softer inflation, lower-than-expected interest rates and a relatively imminent pause to the US Federal Reserve’s rate hiking cycle. This was all up-ended in February by surprisingly strong economic data, including more widely embedded inflation than previously thought. With the Fed signalling its intention to continue hiking, this sent market uncertainty higher and global asset prices lower, an environment that continued well into March.

Then the emergence of banking sector turmoil sparked by the sudden failure of specialist Silicon Valley Bank and the engineered buyout of Swiss banking giant Credit Suisse by UBS shocked markets even further, with swift central bank and government interventions preventing contagion to other sectors. Gold benefited and risk-off sentiment prevailed as global financial stocks sold off. Central banks suddenly had an even tougher policy balancing act, having to choose between their duties of fighting inflation, safeguarding national banking systems and supporting growth and employment. Ironically, this led back to more positive expectations of lower interest rates and sooner-than-expected rate pauses.

In fact, the US Fed hiked by a measured 25bps in March, as expected, as did the Bank of England (BOE), while the European Central Bank (ECB) and SA Reserve Bank (SARB) announced relatively robust 50bp increases given their higher inflation threats. Looking back, investment managers have rarely seen such sharp changes in market views in such a short period of time. US Treasury bonds, for example, experienced high volatility of around 10%, with the 10-year UST yield falling by 50bps from around 4.0% to 3.5% between February and March – an exceptionally big move in that market.

While the growth outlook improved in several key economies, making equities more attractive, risk aversion still made itself apparent over the quarter. Global equity returns outperformed bonds, while developed equity markets outperformed emerging equity markets. For the three months ended 31 March 2023, the MSCI All Country World Index returned 7.3%, the MSCI World Index (developed markets) delivered 7.7%, and the MSCI Emerging Markets Index produced 4.0% (all in US$). Bonds also posted meaningful gains: the Bloomberg Global Aggregate Bond Index delivered 3.0% (in US$). Global property stocks continued to generate among the weakest returns, with the FTSE EPRA/NAREIT Global REIT Index returning 1.4% (US$).

In South Africa, the equity market was dented by risk aversion and weakness in Listed Property and Resources stocks during the quarter, but buoyed by Industrial shares. The FTSE/JSE All Share Index (ALSI) returned 5.2% in Q1, while the more locally exposed Capped SWIX delivered 2.4% (both in rands). Industrial counters returned 13.6%, while Financials produced 0.4%, Resources -4.4% (Resources 10 Index) and the All Property Index -4.8% (all in rands).

For the quarter, SA nominal bonds (the FTSE/JSE All Bond Index) delivered 3.4% in rands, while inflation-linked bonds (ILBs) produced 0.9% and cash returned 1.7%. Finally, despite some late-March gains on the back of the SARB’s larger-than-expected rate hike, the rand moved weaker against the major global currencies, losing 4.8% against the broadly weaker US$, 7.3% against UK sterling and 6.5% versus the euro over the quarter.

|

Asset class |

Total return Q1 2023 (Rand and US$) |

|

SA equity – FTSE/JSE All Share Index (Rand) |

5.2% |

|

SA equity – FTSE/JSE Capped SWIX All Share (Rand) |

2.4% |

|

SA listed property – FTSE/JSE All Property Index (Rand) |

-4.8% |

|

SA bonds – FTSE/JSE All Bond Index (Rand) |

3.4% |

|

SA inflation-linked bonds – FTSE/JSE Inflation-Linked Index (Rand) |

0.9% |

|

SA cash - STeFI Composite Index (Rand) |

1.7% |

|

Global equity – MSCI All Country World (Total, US$ net) |

7.3% |

|

Global equity – MSCI World (Developed) (US$ net) |

7.7% |

|

Global equity – MSCI Emerging Markets (US$ net) |

4.0% |

|

Global bonds – Bloomberg Global Agg Bond Index (US$ net) |

3.0% |

|

Global property – FTSE EPRA/NAREIT Global REIT Index (US$ net) |

1.4% |

Source: M&G Investments, Bloomberg, data to 31 March 2023

In the US, the US Fed hiked its repo rate by 25bps at both its February and March meetings, moves that were expected by the market. However, uncertainty was created by surprisingly robust economic data, including strong retail sales data, a higher-than-expected January CPI at 6.4% y/y, and a still-strong jobs market. February’s core CPI, at 5.5% y/y, showed inflation was more deeply entrenched than thought. This data, combined with hawkish language from the US Fed, led investors to expect higher interest rates for longer and sparked global equity and bond sell-offs.

This bearish sentiment was later reversed by the global banking turmoil, which led investors to expect central banks to move less aggressively in their rate increases in order to support the banking sector. While banking stocks did sell off, March’s confirmed “small” 25bp increase by the Fed appeared to reinforce the idea that US rate hikes might be close to an end, and that therefore uncertainty had eased to an extent. Upward revisions to US growth forecasts, and for other key economies, also reinforced the broadly more positive outlook by the end of the quarter. US equity returns were positive for Q1: in US$, the Dow Jones produced 0.9%, the Nasdaq delivered 17.0%, and the S&P 500 returned 7.5%.

In the UK, the Bank of England (BoE) raised its key interest rate by a total of 50bps in Q1 to 4.25%, in line with forecasts, reaching its highest level in 14 years. February CPI came in unexpectedly high at 10.4% y/y, and financial markets are still pricing in another 25-50bps of increases by August 2023. With January GDP growth reported at 0.3% m/m, the economy has so far avoided the recession that had been forecast, growing more quickly than expected and having picked up pace from the 0% recorded in the last quarter of 2022.

Meanwhile, Chancellor of the Exchequer Jeremy Hunt’s three-year Spring Budget introduced higher taxes and spending, sparking labour protests on Budget day in mid-March. However, it also contained improved economic growth projections, including no recession for 2023. The UK economy is the only one of the G-7 not to have recovered to its pre-pandemic size. For Q1 2023, the FTSE 100 returned 6.4% in US$.

Despite banking sector weakness, the ECB continued its relatively aggressive pace of rate hikes in Q1 as it found itself faced with still-high, albeit falling, levels of inflation. It hiked by 50bps in March as CPI surprised to the upside at 8.5% y/y in February versus 8.2% expected, with core CPI (excluding food and energy) at 5.6% y/y versus 5.3% expected. The bank also signalled its readiness to supply the banking system with extra liquidity should it be required. Financial markets now expect further hikes will be less aggressive going forward, having cut back their forecasts by a full 1.0%.

In February the European Commission revised upward its 2023 GDP growth forecast for the region to 0.8% from 0.3% previously, on the back of falling energy prices, government policy support and resilient household spending. Meanwhile, large and widespread public protests and strikes arose across France in March as a result of French President Emmanuel Macron’s public pension reform, which sees the retirement age rise from 62 to 64. In European equity markets, France’s CAC 40 returned 15.4% and Germany’s DAX delivered 14.3% (in US$) in Q1.

Japan continued its recovery from the pandemic during Q1, as outgoing BOJ Governor Kuroda left interest rates unchanged at a supportive -0.1% after having implemented an effective 25bp interest rate hike in December by lifting the country’s fixed 10-year bond yield trading range. The market expects new Governor Eueda, who takes over in April, to also adjust the yield range wider without changing the base interest rate. Meanwhile, February CPI fell to 3.3% y/y from a 40-year high of 4.3% in March. Price increases have been driven by strong consumer demand, higher commodity prices and a weaker yen. Japanese GDP grew 1.1% in 2022, with a 1.3% expansion expected in 2023 on the back of stronger consumer demand, the government’s October 2022 fiscal support package, rising tourism numbers and supply chain improvements. The Nikkei returned 7.6% in US$ for the quarter.

China also continued its recovery from its strict Covid-19 lockdown in Q1 2023, having posted GDP growth of only 2.0% in 2022. The government set a conservative 5% growth target for 2023, with the IMF forecasting 5.2%, which would account for around 30% of global growth for the year. Pent-up consumer demand is driving the current expansion, along with consumer services, while the property sector remains weak.

The PBOC left interest rates steady in Q1 to support the recovery, while also implementing a surprise cut to bank reserve requirements to support liquidity and steady any nervousness associated with global banks. The ongoing monetary policy divergence between China and the US has kept pressure on the yuan and caused some capital to leave the country. Hong Kong’s Hang Seng produced 2.8% for the quarter while the MSCI China returned 4.7%, both in US$.

Larger emerging equity markets posted a broad range of returns over the quarter, led by South Korea’s KOSPI with a 7.7% performance, and the MSCI China with 4.7% (both in US$). Other countries were in the red as the MSCI South Africa delivered -0.4%, Brazil’s Bovespa -3.3%, the MSCI India -6.3% and Turkey -9.2% (all in US$).

The oil price fell during the quarter on the back of expected lower demand as global growth slowed, and improved supply. Brent crude oil lost approximately 7% in US$ terms, ending the quarter at roughly US$80 per barrel after having fallen as low as US$72 per barrel in mid-March. Other commodity prices were mixed in Q1 amid the uncertain sentiment, with gold the largest beneficiary. Nickel was the largest loser, down 24.2%, while zinc lost 3.9% and aluminium fell 1.0%, while copper gained 6.5%. Among precious metals, gold rose 8.0%, but platinum lost 7.6% and palladium was down 18.5%.

South Africa

In South Africa, the SARB surprised with a larger-than-expected 50bp interest rate hike on 30 March, citing strong inflationary pressures from food, administered prices and a depreciating rand. February CPI came in at 7.0% % y/y, aided by substantial increases in food, transport and medical services prices. Many had thought the Bank would follow the US and UK with a 25bp rise, especially given very weak local economic growth: Stats SA reported that Q4 2022 GDP contracted by 1.3%, more than expected, due to intensifying load-shedding. At the same time, National Treasury revised downward its projection for annual real GDP growth, now expected to average 1.4% from 2023 to 2025, versus 1.6% previously.

The 50bp rate increase did help to reinforce the SARB’s global credibility, while the rand reacted by strengthening below the key R18/1USD level. The SA forward rate market is now pricing in a further 50bps in interest rate hikes from the SARB this year before the central bank pauses and then starts cutting rates again. Meanwhile, S&P Global downgraded the sovereign credit rating outlook to stable from positive, citing load-shedding and the fragile economy as the primary drivers.

Also during the quarter, investors welcomed the 2023 National Budget’s improved fiscal trajectory and the government’s plans for Eskom debt relief, as markets reacted marginally favourably. Eskom remained in the spotlight for much of the period as its departing CEO reported high levels of corruption within the utility, prompting more intensive investigations from journalists and the government.

Meanwhile, South Africa was grey-listed by financial watchdog FATF, so that more scrutiny of the country’s international transactions is necessary to root out money laundering and financing of terrorism. Higher costs and administrative hurdles will likely result, experts said, and banking shares fell 2% in reaction to the announcement. Bonds and the rand were little moved, however.

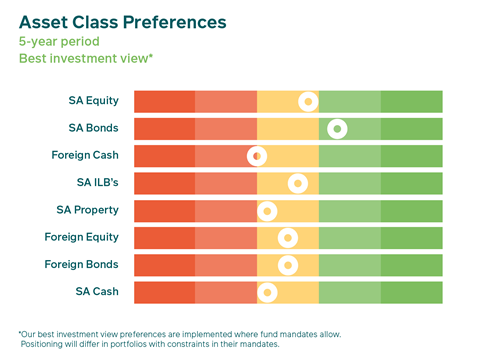

How have our views and portfolio positioning changed in Q1 2023?

Starting with our view on offshore vs local asset allocation, during the quarter we slightly increased our global exposure at the expense of our local cash exposure as a risk mitigation measure.

Within our global holdings, we remained largely neutral in global equities and global bonds, preferring to hold global cash for liquidity purposes, to take advantage of any mis-pricing opportunities that might arise. Despite the volatility over the quarter, corporate earnings were mixed and reasonably resilient, beating expectations in developed markets. With GDP forecasts being revised upwards, equity prices rallied, but in our view it is too soon to be taking large directional bets, since no one knows the extent and depth of any global downturn that might occur.

While global equities are still trading at relatively attractive levels, they became more expensive over the quarter: the MSCI ACWI forward P/E rose to 15.4X from 14.7X previously. Because there are still unresolved questions around risks to earnings going forward, we remain selective and our positions are somewhat muted: we are still leaning away from US equities due to their relatively expensive valuations versus other markets, and are also underweight Canada and Australia. We prefer Japan, China and other emerging markets that are relatively cheap.

Within global bonds, we stayed broadly neutral in our funds and maintained our exposure to 30-year US Treasuries, as well as sovereign EM bond markets where the real yields are high and the currency is trading at fair-to-cheap levels. Real global bond yields are now relatively attractive and offer compensation for the risk involved – that of higher-than-expected interest rate hikes. US Treasuries are also solid diversifiers for SA equity risk.

Our house-view portfolios like the M&G Balanced Fund still favoured SA equities at the end of Q1 2023. Early in the quarter we trimmed our SA equity exposure slightly to take some profit after the roughly 20% rally in the local market in late 2022 and into January, using the profits to increase our SA bond exposure. SA equity valuations (as measured by the 12-month forward Price/Earnings ratio of the FTSE/JSE Capped SWIX Index) re-rated slightly over the quarter, rising from around 9.2X to around 9.5X at quarter-end. Much of this re-rating was attributable to share price gains, as earnings estimates changed only marginally.

Within SA equities, our Industrials exposure was a positive contributor to absolute returns for our house-view portfolios during the quarter, given that sector’s strong performance. Holdings like Naspers, Prosus, Richemont, ABInbev and other stocks with global earnings added value. Detractors from absolute performance stemmed largely from our Resources holdings (Northam Platinum, Glencore, Exxaro, Sasol, for example) and certain bank shares to a lesser extent.

During the quarter, we trimmed our SA listed property exposure further in favour of SA cash, as cash yields became more attractive on a risk-adjusted basis, while property risks remained high. We still prefer exposure to non-property shares that we believe offer better value propositions for less risk. Conditions in the local property sector remain uncertain given the rising local interest rate cycle (many property companies are reliant on finance to expand their portfolios) and relatively weak growth prospects, among other fundamental factors.

Our portfolios also benefitted from our ongoing preference for SA nominal bonds in Q1 2023 due to their positive returns despite a very volatile period. During the quarter we added slightly to our SA bond holdings out of SA equity. The 10-year SA government bond rallied approximately 20bps during the quarter, falling to 10.7% at quarter-end, which is still at a relatively high level on a historic basis. Meanwhile, the 20-year bond lost 20bps, leading to a steepening of the yield curve in the long end, even as the curve below 10 years flattened as a result of the SARB’s interest rate hikes. We continue to believe SA nominal bond valuations remain attractive relative to both other income assets and their own longer-term history and will more than compensate investors for their associated risks.

Although we do not hold inflation-linked bonds (ILBs) to a meaningful degree in our house-view portfolios, we hold them in our real return portfolios such as the M&G Inflation Plus Fund. Here we are marginally favouring these assets after adding more to our holdings in the previous quarter. Their real yields remain relatively attractive (that of the 10-year ILB is at 4.5%) compared to both their own history and our long-run fair value assumption, compared to nominal bonds their valuations are less attractive and they have lower return potential.

Lastly, the SARB’s interest rate hikes during the quarter made SA cash relatively more attractive as an asset class. However, apart from SA property, we still prefer most other local asset classes for the higher real yields available on both an absolute and relative basis. Therefore, our house-view portfolios remained tilted away from SA cash.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter