South Africa

South Africa Namibia

Namibia

Stefan Swanepoel

Equity Analyst

SA Corporate Real Estate: Underrated but improving

This article was first published in the Quarter 4 2021 edition of Consider this. Click here to download the complete edition.

Among the numerous equity investment opportunities in the aftermath of the Coronavirus market crash in March- April 2020, one that stood out for us was listed property group SA Corporate Real Estate (SAC). Long underrated by investors, we had been holding a 15% stake in the company (our maximum) across several of our portfolios since 2018. Yet amid the pandemic lockdown conditions, SAC’s share price was hit even harder than most other companies’, having traded at as much of an 85% discount to its net asset value (NAV) in May 2020. In the ensuing recovery, the counter has more than doubled, delivering strong returns for shareholders, and we believe the company still has the potential to deliver market returns well above-average over the next three to five years, of course with some risk involved. But what has made us confident that this bet will pay off for our clients in the face of considerable doubt by the market?

Active insights

At the time M&G Investments became a shareholder in SAC in 2018, the company was experiencing issues around inadequate governance and conflicts of interest, one reason for the lack of investor confidence. Because of our large stake and active shareholder approach, we were able to step in and appoint several new Board members with suitable experience and a shared vision, as well as seeing the Chairman replaced, all of which helped steady the business. Our in-depth knowledge as an existing and active shareholder in SAC helped us to eliminate some of the uncertainties (and therefore known risks) around investing in the company and the broader property sector when share prices were near their worst levels.

When diversification is a deterrent

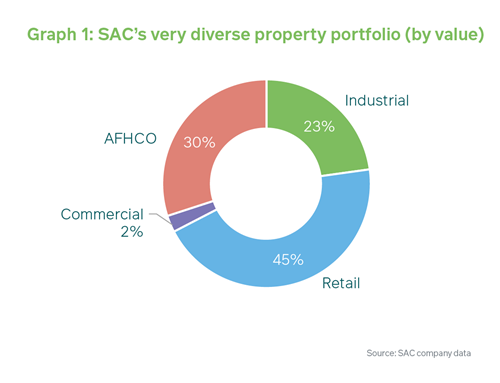

An issue of ongoing concern for investors has been SAC’s lack of focus, as a result of its very wide portfolio diversification across every property segment from office, commercial, retail and residential to even include a small percentage of storage facilities. Graph 1 shows how its largest exposure, to the retail market segment, comprises only 45% of its total property portfolio by value. While normally some degree of asset diversification could be considered an advantage, in the listed property sector owning and managing such disparate property types requires more management time and expertise than most SA property companies possess.

Equally, when it comes to investing in property, investors tend to prefer very focussed businesses specialised in just one property segment where management can build their skills accordingly.

This allows the investor to allocate their capital carefully across different property segments, depending on the prevailing market conditions, as one segment will outperform or lag another in different stages of the business cycle.

SAC’s ownership of a portfolio of 66 residential properties in the inner city of Johannesburg (including large blocks of flats) was of particular concern due to SA investors’ scepticism over their residential business model. This applied notably to their short lease terms of only one year (compared to shopping centre leases of 4-5 years, commercial leases of 2-3 years, and industrial leases of up to 10 years), as well as the specialised residential broker expertise required to manage them efficiently.

This portfolio stemmed from the company’s 2014 acquisition of the AFHCO Group, a business that invests in, develops, and manages affordable housing and commercial property in Johannesburg. Although accounting for 30% of SAC’s total portfolio by value, the source of its profits has not been well understood by the market, along with an existing perception that its large number of properties and tenants consumed a disproportionate amount of staff time and attention. Sourcing new individual residents, verifying their creditworthiness and collecting rents are all very different skills than managing commercial shopping mall tenants and ensuring they are trading at the correct sales densities. These inner-city properties are also partially reliant on migrant workers as tenants, a group that was particularly hurt by the pandemic.

Another factor weighing on the value of SAC’s portfolio had been that quite a few of the leases for its industrial properties were coming to an end, with expectations that renewals would come in at lower levels (called negative reversions).

Going smaller but stronger

Since 2018, M&G Investments, along with other shareholders, had been urging SAC management to dispose of their non-core assets across various segments and use the proceeds to pay down debt. This became one of the company’s top priorities over the past three years, a plan that was accelerated by the Coronavirus crisis. It set about selling some of its office space (the weakest property segment during the pandemic), converting some offices into storage space (the strongest property segment during the pandemic), and breaking up some of its larger offices into smaller, more affordable offices that have been easier to lease. It also disposed of some of its non-core retail properties in outlying areas, as well as some industrial concerns To date, SAC has sold over 10% of its property portfolio, accumulating proceeds of around R1.8 billion which allowed it to strengthen its balance sheet. They were far more successful than expected given the depressed economic conditions in which the disposals took place, proving able to command prices at an average discount of only 2% to the properties’ book value.

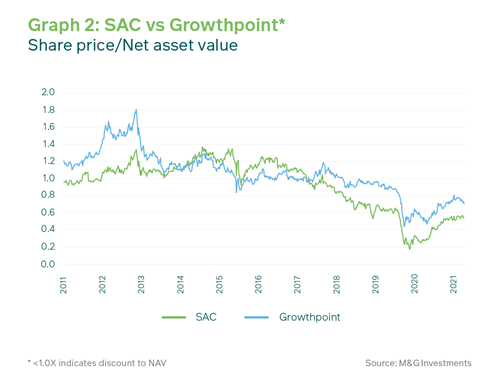

And this came when SAC’s overall company valuation (as measured by its share price/NAV ratio) was still at a deep discount. As Graph 2 shows, it was trading between an 85%-46% discount as the listed property market gradually recovered from the worst effects of the Coronavirus lockdowns, compared to a higher- quality company like Growthpoint’s discount of between 57%-30% since March 2020. M&G Investments bought SAC shares for the M&G Equity Fund at around a 75% discount, in the knowledge that the company’s balance sheet strength was improving, its portfolio was being simplified while retaining the best assets (thereby improving its overall portfolio quality), and that company management was aligned behind further improvements.

Other positive considerations for our analysts and portfolio managers regarding SAC’s investability included:

- SAC has less office exposure than the average listed property company, the segment worst hit by the pandemic.

- It owns a strong selection of industrial properties in very well-located nodes. For example, it owns and runs a state-of-the-art facility in Johannesburg for specialised, high-quality tenants like

- Its retail portfolio has a distinct bias towards smaller neighbourhood convenience centres, which benefitted from consumer spending during the pandemic compared to larger, regional or super-regional shopping malls.

- It has a robust loan-to-value (LTV) ratio at 38%, lower than the sector average of 50%, due to its portfolio structure of smaller assets combined with a larger pool of unencumbered assets. This allows management to be flexible with their financing options.

Taken together, all these factors reduced the risk of investing in SAC, and the substantial discount at which the shares were purchased gave us a large margin of error as investors. Since buying the shares, the share price has doubled, producing above- market returns for clients of the M&G Equity Fund (and other client portfolios).

SAC in the July riots

Properties owned by SAC were among the hardest hit by the riots in KwaZulu Natal and Johannesburg: one of its prime developments, the popular Springfield Value Mart outlet mall in KZN, featured at the centre of the damage and looting. Total damages, including loss of income, were estimated at approximately R560 million, with R557 million relating to its retail shopping centres in KwaZulu-Natal, R700,000 to its industrial properties and R75,000 to its inner-city properties in Johannesburg.

Luckily SAC was covered by SASRIA for the full R560 million of losses of both property and income (not true for all SA companies), representing 3.1% of its total assets. In fact, at the time of writing, trading had resumed at all of the company’s other retail shopping centres where the damage was relatively minor. And the remaining restoration was expected to have been completed by October. For Springfield in particular, it will soon receive a more extensive upgrade than previously planned, to higher standards, with no problems foreseen for the reintroduction of its larger retail tenants due to its popular location. SAC will even be saving money on its planned capital spending for the centre. It expects to complete the rebuilding project by October 2022.

What are the prospects for SAC amid a subdued economy?

Over the near-term, SAC’s plans include spinning off its remaining commercial and non-core residential assets, slimming down further to focus on its industrial, retail and some remaining residential properties. Management has also stated its intention to pay down more debt, consequently reducing the company’s interest payments and further improving its LTV ratio and balance sheet. And importantly for investors, SAC is committed to paying out 75% of its taxable earnings as shareholder distributions, in line with its regulatory requirements as a Real Estate Investment Trust (REIT).

In our view, with the industrial property market segment able to command very long-term leases, SAC should be able to improve its returns going forward. However, investors continue to be concerned about ongoing negative reversions for industrial property rentals, which are likely to lead to lower operating income for the group in the near-term, as well as other issues like still- weak retail spending (in absolute terms). This is reflected in the company’s share price continuing to trade at a substantial 46% discount to its book value, deeper than that of Growthpoint, for example. This gives SAC the potential to experience a bigger re-rating than its larger, higher-quality counterparts.

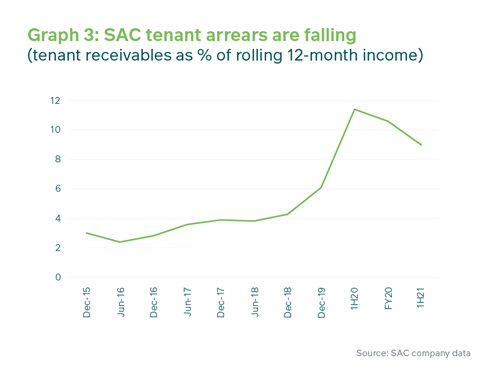

Over time and as the local economy continues to recover, we expect the current elevated level of vacancies will normalise across the sector. For SAC in particular it should fall to around 2% of the group’s rental income. At the same time, rental collections will improve as landlords no longer have to forgive portions of rents, and tenant arrears, already improving, will continue to do so, as shown in Graph 3.

M&G Investments believes that, given the above factors and developments, SAC has a brighter future ahead for itself and its investors. Like surprisingly many South African companies, it is emerging from the Coronavirus crisis as a stronger entity. It is better managed, more focused and efficient, building greater capacity in its teams and, we feel, headed in the right direction. And as a key attribute for us as valuation-based investment managers, it is still attractively priced, with fewer company and sector risks now than in the past. For us, the market is still pricing excessive risk into SAC’s share price, which gives our portfolios, as holders of the stock, greater potential for outperformance going forward through a combination of both capital value growth and re-rating.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter