South Africa

South Africa Namibia

Namibia

Pieter Hugo

Chief Client and Distribution Officer

Deciding whether to go offshore? Don’t just look at the rand

Too many investors only consider the rand’s value when they take money offshore -- usually after it’s plunged

The first half of 2016 has seen a rush by many investors to take funds offshore, precipitated by the sharp depreciation of the rand following the Nenegate debacle in December 2015. Unfortunately, South Africans have a history of panicking when the rand weakens sharply and responding by taking money offshore. The rand is a highly emotive factor, so investors’ immediate focus is often solely on the level of the rand, and not whether an offshore investment actually makes sense from a valuation perspective – they ignore whether the South African assets they are selling and the foreign assets they are buying at the time are cheap or expensive. They also tend to forget about the impact on their overall portfolio.

What economics tells us should happen to the rand

It’s important to remember that we should expect the rand to depreciate against the US dollar over time: on a purchasing power parity (PPP) basis, economic theory tells us that the rand should depreciate by roughly 4% p.a. versus the US dollar over time, based on the inflation differential between the two countries. Surprisingly, it has averaged about 4% p.a. over the longer term, with wide variations over shorter time periods.

How offshore investments fared

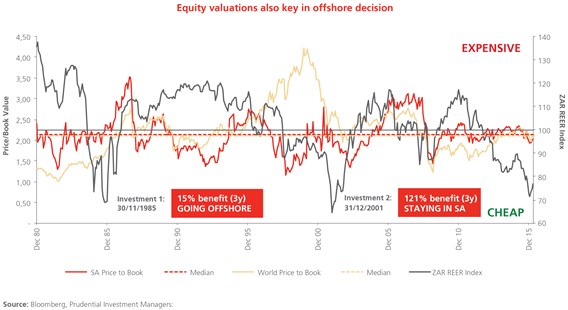

So did investors who panicked after the previous big rand depreciations - in November 1985 and December 2001 – benefit from moving offshore? A look at the equity market and currency valuations at the time tells us the results were mixed. In the graph, the grey line depicts the value of the rand on a real effective exchange rate (REER) basis against a basket of currencies. It shows that, in the 1985 episode, investors would have sold the rand at about 30% cheap, sold SA equities at roughly fair value (as shown by the red line on a share price/book value basis) and bought offshore equities at about a 25% discount (depicted by the yellow line). After three years, we estimate that this would have resulted in about a 15% benefit to investors relative to staying in SA.

However, in 2001 investors did not fare as well. Not only did they sell SA equity somewhat cheap, they also bought offshore equity at 10-20% expensive levels, and they sold the rand at an exceptionally cheap 35-40% discount. We estimate that, after three years, investors would have benefited by approximately 121% to have stayed in the local market instead of going offshore.

Following the Nenegate-inspired depreciation, the graph illustrates that both global and South African equities have been marginally expensive, and the rand has been 20%-25% cheap. However, the rand has strengthened in recent months, so our calculations show that an investor who moved R100,000 offshore at the end of December 2015, following Nenegate, would now have R94,533 (as of the end of June 2016), whereas a South African equity investment would be worth R104,324, nearly R10,000 more. This is a large difference over a short time period of six months - but it’s still too soon to know if an offshore move has paid off. A three-year timeframe would be more appropriate.

A holistic view is needed

It’s clear from these examples of past experience that investors looking to take money offshore in the current environment need to understand asset valuations at the time, as well as the value of the rand, when making their decision. And of course they should take a holistic view of the impact on their overall portfolio. Although it is the vagaries of the rand that capture all the attention, it is not the only factor that matters in such an important decision.

To read the full article, look out for it in the spring edition of Consider thismagazine.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter