South Africa

South Africa Namibia

Namibia

David Knee

Chief Investment Officer

Market Observations: Q4 2021

The final quarter of 2021 was a very positive one for South African investors and M&G Investments’ clients thanks to rallies in developed equity markets around the globe and in South Africa -- investors looked past negative developments like the higher uncertainty posed by the Omicron variant of the Coronavirus to push many bourses to fresh record highs. Amid this risk-on sentiment, many of the world’s equity markets recorded impressive returns in 2021. However, emerging market equities lost ground in Q4, with the broad MSCI Emerging Markets Index ending the year in the red, dragged down by large losses in China and Turkey. Equally, global bonds posted negative returns in Q4 and for the year as a whole as many central banks finally signalled or started to pare back on their ultra-easy monetary policies by trimming asset purchases and/or hiking interest rates to fight rising inflation.

In the US, the most obvious emerging headwind to growth was the rapid spread of the Omicron variant, which stretched local health services and disrupted economic activity around the country. In another significant development, the Federal Reserve (Fed) shifted to a more aggressive inflation-fighting stance, doubling the pace of its planned reduction in asset purchases and also bringing forward the timing of its expected rate hikes – the Fed now sees an average of three 0.25% rate hikes in 2022. This came as US CPI jumped to 6.8% y/y in November, the highest since 1982, while producer prices (PPI) soared to 9.6% y/y, fuelled by energy price increases and ongoing supply chain blockages. And on the government spending front, Congressional opposition to President Biden’s nearly US$2 trillion “Build Back Better” programme meant spending delays and likely cutbacks in the programme’s total future injection into the US economy.

However, investors largely looked through these negative developments, instead focusing on indications of Omicron’s less severe nature and the government’s decision not to impose very strict lockdown measures to combat it. They were also encouraged by reports of some progress in developing a “universal” vaccine to help prevent all future variants of Covid-19. Markets also took comfort from the robust pace of the US recovery. The Conference Board estimated US GDP growth at 6.5% y/y in Q4 of 2021, and 5.6% for the full year, the highest in decades. Consensus expectations for 2022 averaged around 4.0%, still above its longer-term average. Meanwhile, the US unemployment rate continued to fall, reaching 4.2% in November from 4.6% in October, comfortably beating market expectations of 4.5%. And although December Manufacturing PMI decreased to 57.8 from 58.3 the previous month as factory production remained constrained, the survey encouragingly also indicated that supply constraints showed signs of easing.

Equally important for the equity market, US companies continued to report impressive earnings growth in Q4 amid the sharp rebound in consumer and government spending, helped by a low base effect in 2020: For 2021 as a whole, FactSet estimated S&P 500 earnings growth of some 45% y/y. The S&P 500 delivered an impressive 11.0% return in Q4 and 28.7% in 2021, the Dow Jones Industrial 30 7.9% and 20.9%, and the technology-heavy Nasdaq Composite 8.4% and 22.2% (all in US$).

Both the Bank of England (BoE) and the European Central Bank (ECB) followed the US Fed’s policy tightening during the quarter, but to a lesser extent. The BoE hiked its base interest rate by 15bps to 0.25% amid a jump in CPI to 5.1% y/y in November, its highest in 10 years. PPI also accelerated to 9.1% in November, much higher than the 8.3% consensus forecast. In December the UK’s total GDP was only 0.5% below its pre-Coronavirus levels, and the OECD expects it to grow by 6.9% in 2021 before slowing to 4.7% in 2022 and 2.1% in 2023.

Meanwhile, the ECB left its base rate unchanged at its December meeting, but cut its bond buying as planned, trying to balance inflation (at a 25-year high of 4.9% y/y) with Omicron’s negative impact on economic growth. The OECD is projecting that Euro-area GDP growth will record a strong rebound of 5.3% for 2021 and then decelerate to 4.3% in 2022 and 2.5% in 2023.

For Q4, the UK’s FTSE 100 returned 5.2%, Germany’s DAX 1.8% and France’s CAC 40 7.8%. For the year, the UK’s FTSE 100 delivered 17.4%, Germany’s DAX 6.7% and France’s CAC 40 22.6% (all in US$).

The Japanese economy, which has been particularly hard-hit by the pandemic and slower to recover than other large economies, is expected to post growth of only 1.8% in 2021 before accelerating to 3.4% in 2022. In 2023, however, the OECD sees it slowing to only 1.1%. With inflation still well below the Bank of Japan’s 2.0% target, the BOJ kept its interest rates ultra-low in December and extended its support for small companies, promising to maintain its dovish stance as necessary.

In China, institutions including the World Bank lowered their forecasts for the country’s 2021 GDP growth to around 8.0%, the result of a slowdown towards year-end that was partly due to subdued consumer spending, Covid outbreaks and very strict government containment measures, as well as a slumping property market and constrained production activity. With the Chinese economic cycle ahead of Western countries’, its 2022 GDP growth is now expected at around 5%, the lowest in decades. The People’s Bank of China (PBoC) cut its one-year loan prime rate for businesses and households to 3.8% from 3.85% in a move to bolster growth, even as its lower reserve requirements for banks also took effect. Manufacturing PMI rose slightly to 50.9 in December in a sign of rising output and easing supply constraints, while retail sales surprised to the downside at 3.9% y/y, versus the 4.6% y/y forecast.

Japan’s Nikkei 225 fell sharply in Q4 with a -5.1% return, and was one of the few large equity markets to record a loss in 2021 at -4.4% in US$. Other prominent bourses in the red were China and Hong Kong due to the government’s regulatory and democratic crackdowns, and strict anti-Covid measures. The MSCI China lost 6.1% in Q4 and delivered -21.6% for 2021, while Hong Kong’s Hang Seng fell 4.8% for the quarter and posted a -12.3% return in 2021 (all in US$).

Among other large emerging equity markets, in US$ terms, the MSCI Turkey was the worst performer in Q4 with a -11.1% return, while the MSCI Russia posted -9.0% and Brazil’s Bovespa delivered -7.6%. Less in the red were South Korea’s KOSPI at -2.3%, the MSCI South Africa with -0.4% and the MSCI India with -0.1% (all in US$). For 2021 in total, the Indian and Russian equity markets were the standout performers with total returns of 26.7% and 20.0% respectively, while China and Turkey were the biggest losers, delivering -27.8% and -21.6% respectively to investors for the year.

The spot price of Brent crude oil fell 0.9% in Q4, but still rose some 50% over the course of 2021, ending the year at around US$79 per barrel and fuelling global inflation. Other commodity prices were mostly stronger over the quarter: zinc gained 20.4%, nickel 15.1%, lead 10.1% and copper 7.2%, while aluminium lost 1.6%. However, aluminium was among the strongest gainers in 2021, up 41.9%, even as copper gained 25.2%, zinc 33.3%, and nickel 26.5%. Precious metals were much more subdued for the year, with palladium down 20% in 2021, platinum losing 9.4% and gold falling 3.4%.

South Africa

In line with market expectations, the South African Reserve Bank (SARB) hiked the repo rate by 25bps to 3.75% in November. Data showed CPI rose to 5.5% y/y and PPI hit a 10-year high of 9.6% y/y in November, largely driven by higher fuel prices, reinforcing expectations for more interest rate hikes from the SARB in 2022. The MPC’s latest forecasts show a gradual rate hiking cycle, with the repo rate reaching approximately 5.0% by December 2022, 6.0% at the end of 2023 and 6.75% by end-2024.

South Africa’s GDP growth slowed to 2.9% y/y in Q3, contracting by 1.5% on a quarterly basis due to the harsh impact that July’s riots and tighter lockdowns for the Coronavirus had on consumer spending, investment and production. Forecasts show a consensus of around 5.1% growth for 2021, falling to around 2.0% in 2022, as the economy faces more headwinds such as the continuation of the Coronavirus pandemic, slowing global growth, rising interest rates, further power constraints and lower government spending, among others. Commodity prices, which provided a strong underpin to SARS revenue collections and the local equity market in 2021, are likely to be less supportive in 2022. The SARB’s expectations are for growth of 5.3% in 2021, falling to 1.7% in 2022 and 1.8% in 2023.

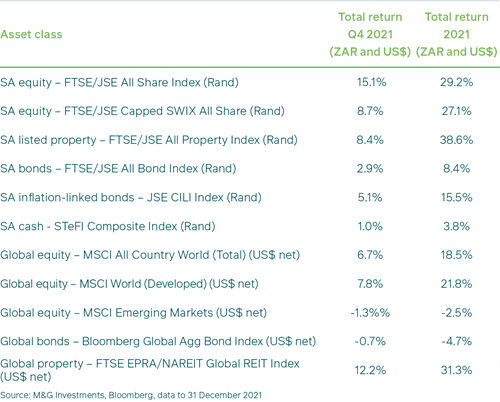

SA equities posted robust Q4 gains, with the FTSE/JSE ALSI returning 15.1%.

The FTSE/JSE Capped SWIX ALSI, which we use as the equity benchmark for most of our client mandates, returned 8.7%. Gains were led by the globally-exposed Resources and Industrial sectors, which delivered 22.2% and 16.1% respectively, while the All Property Index produced 8.4% and Financials 2.5%.

For the 2021 year, the ALSI returned the most in 10 years at 29.2% thanks to strong performances from Listed Property and Resources (up 38.6% and 32.4% respectively).The FTSE/JSE Capped SWIX ALSI delivered 27.1% for the year, Financials produced 29.6% and Industrials returned 26.5%.

In what was a generally weak year globally for bonds as interest rates started to rise, SA bonds delivered 2.9% in Q4 and registered a world-beating 8.4% annual return in rands in 2021 in total. SA inflation linked-bonds delivered 5.1% in Q4 and 15.5% for the year, outperforming their nominal counterparts, and cash (as measured by the STeFI Composite) posted returns of 1.0% in Q4 and 3.8% for the year.

Finally, the rand lost ground against the major currencies in Q4, losing 6.2% against a weak US dollar and 6.4% against the pound sterling, as well as 3.9% against the euro. For the year it depreciated 9.1% versus the US dollar, 8.0% versus sterling and 0.9% against the euro.

How have our views and portfolio positioning changed?

Starting with our view on offshore asset allocation, we maintained our portfolio positioning favouring global cash over global equities and bonds in order to keep risk relatively low and take advantage of market mis-pricing episodes that might arise. Within our global equity positioning, we remained cautious in our exposure to US equities, as this market continued to be expensive compared to most other countries. Instead, our portfolios favour selected European and other developed market equities, and some emerging market equities. We have been aiming to position the portfolios with higher weightings of very high-returning global assets while maintaining a mix of assets that have diversified return profiles, thereby cushioning them against unforeseen shocks.

At the same time, we kept a marginal preference for global government bonds in Q4 compared to investment grade corporate credit, keeping our small selective exposure to emerging market government bonds as yields remained attractive. We believe that corporate yield spreads are not sufficiently high for the risk involved.

Our best investment view portfolios like the M&G Balanced Fund still heavily favoured SA equities at the end of Q4. After de-rating for much of the year, SA equity market valuations (as measured by the 12-month forward Price/Earnings ratio of the FTSE/JSE Capped SWIX Index) finally re-rated slightly over the quarter, moving up from around 9.2X to around 9.5X at quarter-end. Equity price gains outpaced earnings revisions, but investors remain skeptical over the sustainability of local earnings growth and the country’s economic growth. This increase in valuations was too small to cause us to lower our allocation to SA equity.

Within SA equities, in broad terms our exposure to large global companies worked in our favour over the quarter and in 2021 as a whole. However, even more notable was our broad diversification of holdings that added value for clients: the top equity contributions to our House View portfolios for the year came from our overweight holdings in MTN, Investec, PPC, Sasol, Richemont and Textainer. Meanwhile, top equity detractors included our holdings in Multichoice, Standard Bank, Foschini and British American Tobacco, plus our underweights in Aspen, Capitec and Shoprite.

We continued with our neutral positioning in SA listed property in Q4 2021, having shifted some exposure away from the higher-valued property counters into more attractively-valued companies with higher return prospects in Q3, in recognition that risks in the sector have been improving. Although listed property does offer somewhat better value than our estimated fair value for the sector, at around 7.5% versus 6.0%, within SA equities we prefer other shares that we consider offer better value propositions for less risk.

Listed property proved to be the best-performing sector (and asset class) in 2021, recording a 38.6% return. The quality of the sector is improving, as dividend yields have proved fairly robust and companies have built safety into their balance sheets by not paying out excessive distributions. This leaves room for further re-rating. Property also offers diversification benefits. However, as with the previous quarter we are mindful that listed property is a lagging sector in the cycle, as earnings are usually only impacted negatively once rental contracts come to an end and new rents are set at lower levels (negative reversions) – and this is still happening. So while the logistics and self-storage segments have been the most resilient and are performing well, retail is still weak and the office segment even weaker, plagued by high vacancies.

Our portfolios benefited from our ongoing preference for SA nominal bonds in Q4 (and the year as a whole) thanks to their resilient performance and the flattening of the SA yield curve in the wake of the SARB’s rate hike. With inflation proving to be less of a risk than expected, and the SARB’s own rate hike projections more dovish than previously priced into the market, during the quarter bond investors tempered their own rate-hike expectations and aligned with the SARB’s view. As in Q3 we prefer the 7-12-year area of the curve, where relative valuations have become more attractive, but are also still holding bonds of 12-years and longer that have outperformed. We still believe nominal bonds remain attractive relative to both other income assets and their own longer-term history and will more than compensate investors for their associated risks.

Inflation-linked bonds (ILBs) outperformed their nominal counterparts during the quarter by some 2.2% (220 basis points), extending their phenomenal run for 2021. Although we are not holding ILBs in our best investment view portfolios, we do hold them in our real return portfolios like the M&G Inflation Plus Fund. As in Q3, the outperformance by ILBs in Q4 led us to take some further profits in our real return portfolios and buy more nominal bonds during the quarter, as the latter’s relative valuation became more favorable. Although we reduced our exposure slightly, we still believe that ILB real yields remain relatively attractive compared to their own history and our long-run fair value assumption of 2.5%. In Q4 the gap between ILB and cash real yields narrowed as a result of the SARB’s rate hike and the fall in ILB yields.

Lastly, despite the SARB’s 25bp interest rate hike, our best investment view portfolios remained heavily tilted away from SA cash in Q4 as our least preferred asset class, given the extremely low base rate off which the SARB hiked. Prospective real returns are still negative and other SA assets more attractive on a relative basis.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter