South Africa

South Africa Namibia

Namibia

Yusuf Mowlana

Portfolio Manager

Fortress Real Estate: Improvements, problems and opportunities

Investors following recent movements in the South African listed property sector will have noted the conclusion of a deal in which Fortress Real Estate Investments (Fortress) exchanged 0.060207 Nepi Rockcastle (Nepi) shares for every Fortress ‘B’ share outstanding. This equated to roughly one-third of Fortress’s holding in the Central and Eastern European retail landlord.

The company had been mired in controversy over a number of years as it pursued unconventional accounting policies which, on the face of it, created a more conservative earnings base, but had the effect of reducing its distributable earnings, which fell short of the ‘A’ share entitlement for shareholders. This shortfall was interpreted by the company as preventing it from declaring a dividend to A shareholders, notwithstanding the fact that it met the entitlement on conventional accounting policies, being the SA REIT Best Practice standards. More details on Fortress’s conundrum can be found in the article written about the company in October 2022 : https://www.mandg.co.za/insights/articlesreleases/fortress-not-such-a-shareholder-bastion/.

The net effect of the recent transaction is that Fortress’s unwieldy dual unit structure has been collapsed and the A shareholders now own what remains in the company, being the residual Nepi Rockcastle shares, the Eastern European logistics assets and the South African business which comprises retail, logistics/industrial assets and a non-core office portfolio.

Benefits and pitfalls of the deal

Fortress is a core holding of the M&G Property Fund. The deal required careful consideration on behalf of clients, seeing as though we had turned down a similar attempt to collapse the structure when the company last proposed a deal. Critics of the deal would point to the fact that the holders of B shares received a value substantially in excess of the intrinsic value of their B shares in the form of Nepi shares, and that A shareholders who remained invested in the company had to reduce their holding in the more attractive part of the business and also are left with a weaker balance sheet post the deal.

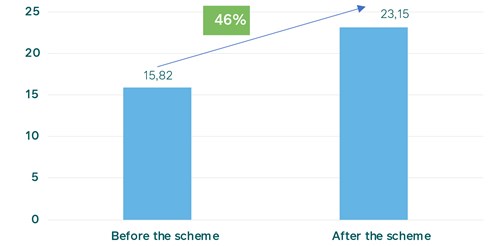

On the other hand, although value was given up to the B holders, the company would be a much simpler investment proposition, and importantly there would remain appropriate value in the company post the deal. Although somewhat theoretical, the former A shareholders enjoyed a substantial uplift of 46% in their claim on the net assets of the business on a per share basis, as shown in Graph 1. This greater claim on the company’s net asset value, together with the single share structure, does provide the former A shareholders with arguably a greater element of downside protection, in our view. Some of the riskier aspects relating to ownership of the A shares were also dispensed with as a consequence of the deal, which was no less of an important consideration than the effect on the company’s valuation.

Graph 1: Net asset value per former Fortress A share improves (Rand per share)

Source: Fortress scheme circular

The problem and the opportunity

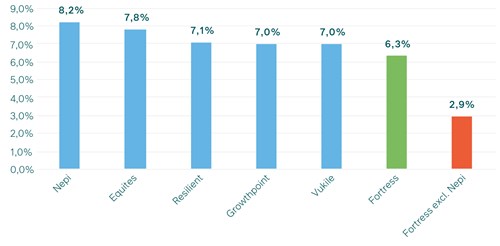

The company’s holding in Nepi has allowed it to operate with somewhat less investor scrutiny over the direct operations of the company, in that much of its positive performance can be attributed to its holding in Nepi, thus obscuring the poor-returning domestic business from full view. An analysis of the company’s balance sheet and earnings from its directly controlled investments suggests that the shareholder capital invested by the company in its own directly-controlled operations, excluding its shareholding in Nepi, is earning far less than it should. A comparative analysis of listed property company NAV yields in Graph 2 demonstrates that R100 of shareholder capital invested in Nepi at book value would earn R8.20 in accounting earnings, R7.80 in Equites and R7 in Vukile1. Excluding Nepi from Fortress’ earnings and book value suggests that the same R100 would earn a mere R2.90 in the hands of the Fortress management team. This analysis would fall flat were the companies markedly different from each other, but they all have overlapping asset classes (retail and logistics) and geographic exposures (South Africa and Europe), thus rendering the comparison appropriate.

Graph 2: Fortress net asset value yields (excl Nepi) fall short of peers

Source: M&G Investments, company data

Among the reasons for this apparent anomaly are the fact that the company employs a great deal of debt – more than other REITs – in its directly owned portfolio. Debt levels relative to the investment property balance, excluding developments and properties held for sale on the balance sheet, stand at 61%. With interest rates having crept up to be in excess of asset yields, it means that equity holders are worse off for having the debt, unless the company can grow its rentals strongly over time. Further, a substantial portion of the company’s net assets are “under-earning” by virtue of being under development and not income-producing.

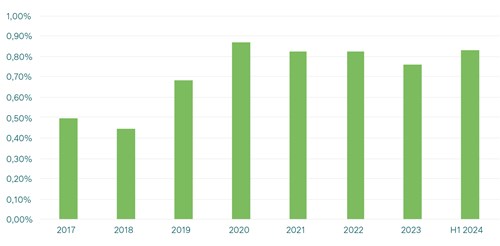

Additionally, relative to its directly-held income-producing asset base, the company’s overheads appear high. The overhead cost has outgrown the asset base by a whopping 68% since 2017, as Graph 3 illustrates, from approximately 0.5% of the investment property balance to over 0.8%. Considering that overheads relating to developments are capitalised to the cost of the development, the company appears to have some upside were it to implement a leaner cost structure.

Graph 3:

Source: M&G Investments, Company data

Lastly, Fortress has lost its REIT status as a consequence of it not paying a dividend. This has resulted in the company incurring a tax charge, which other REITs do not generally incur, and which is therefore unnecessary in our view. In our assessment, the majority of shareholders are ultimately pension fund investors who enjoy the ability to defer income taxes many years into the future. It therefore makes sense for the company to seek REIT status as soon as possible.

To be clear, we view the depressed returns earned by the portion of the business excluding Nepi as an opportunity rather than a problem: management could dispose of assets at book value, as they have done, to pay down debt, thus boosting returns to shareholders in the near term and bringing the company’s capital structure more in line with peers. The upside to shareholders would be very substantial if the company were able to earn a return on shareholders’ net assets in line with peer companies.

Shareholder value creation

Following the elimination of Fortress’s dual share structure, there are further changes to the company that may result in better outcomes for shareholders than have currently been achieved, including:

- Asset disposals to boost returns

As outlined above, the company earns poor returns from its directly-controlled assets. One way to improve returns is to consider disposals of assets to the extent that these can be done at the company’s book value, as the management team have demonstrated in the recent past.

- A return to REIT status

A return to REIT status will serve to reduce the tax burden on the company and improve net returns to the company’s largest shareholders.

- A reduction in overheads

This should be obvious, but a comparative analysis suggests the company carries bloated overhead costs.

- Disciplined and thoughtful capital allocation

Given the low returns earned by the South African core business, it makes little sense to continue to allocate capital to developments. With R100 invested in the SA business currently earning just R2.90, shareholders would be far better off if the company were to prioritise the paydown of its debt. Further, given the large discount to the appraised value of its assets at the time of writing, R100 invested is valued at a fraction of the actual amount invested, and so any developments and reinvestment in the business currently do not add value to shareholders.

In time, it would be appropriate for the company to unbundle its shareholding in Nepi given the fact that Nepi no longer needs to rely on Fortress to support capital raises, and shareholders would prefer a leaner, more focused company.

In conclusion, while not presenting optical relative value to some of its sector peers, with some imagination and intent from the management team, we see significant upside from the improved management of the business for the benefit of shareholders.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter