South Africa

South Africa Namibia

Namibia

Damon Buss

Equity Analyst

Woolworths: The turnaround is gaining traction

This article was first published in the Quarter 3 2022 edition of Consider this. Click here to download the complete edition.

Key take-aways

-

Although Woolworths’ Food division has always performed strongly and is highly regarded, its Fashion, Beauty and Home (FBH) division has struggled in recent years from poor management decisions, poor execution and growing competition in South Africa.

-

Its 2014 acquisition of Australia’s David Jones department stores turned out to be disastrous for the company, due to the high debt levels it assumed and the group’s subsequent poor performance, resulting in large write-offs for Woolworths.

-

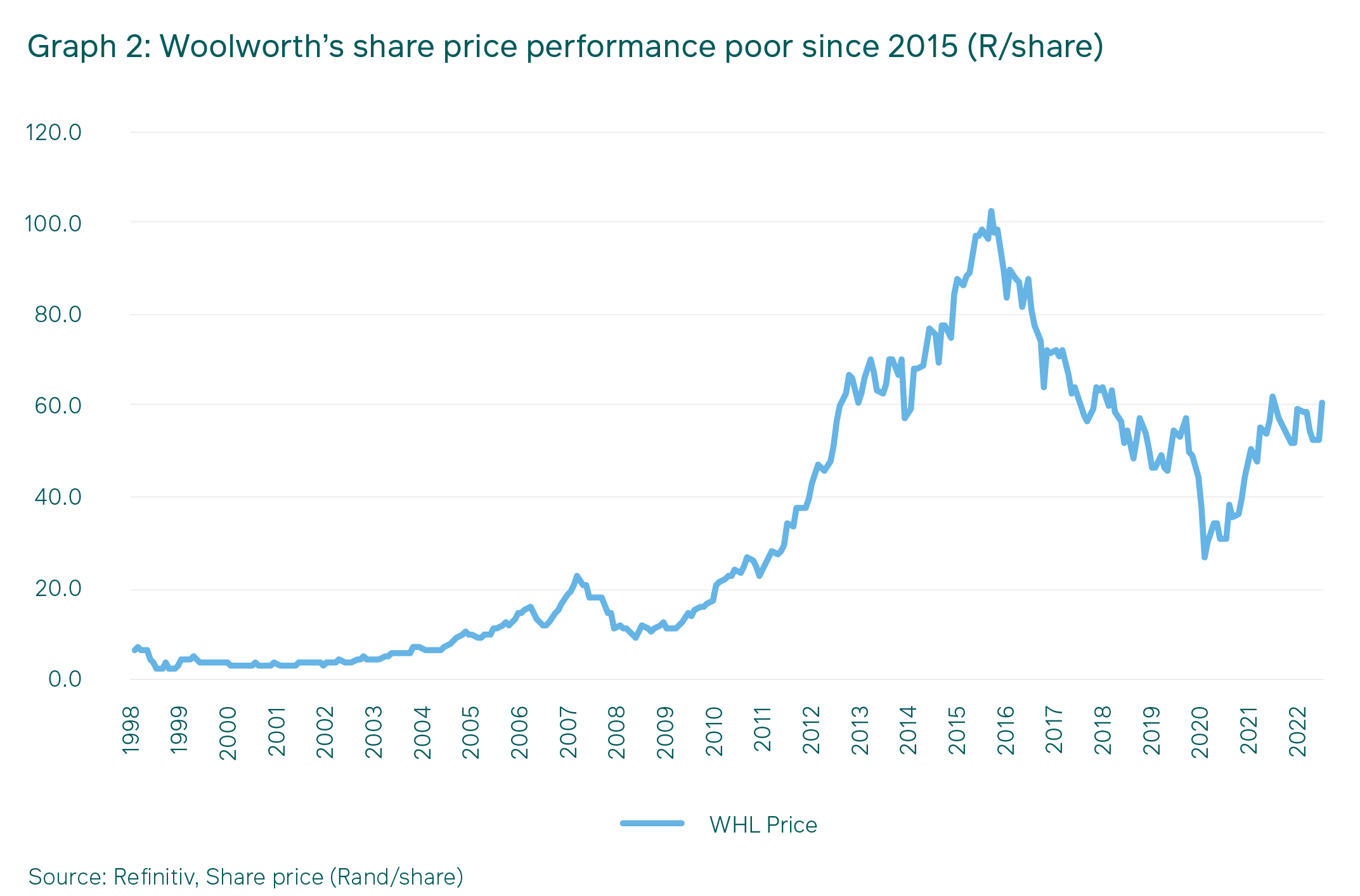

These issues have weighed on the company’s share price, only experiencing a partial recovery from 2020 as the group paid down its debts on the back of the Food division’s strong cash flows and implemented fixes to both its FBH division and David Jones. As a shareholder, we are optimistic that its current turnaround will continue, and that share performance will add value to our client portfolios over the medium term.

Woolworths (WHL) is an iconic brand in South Africa, largely due to the success of its Food business in South Africa, which grew rapidly in the 2000s and early 2010s as it rolled out stores and entrenched itself as one of the leading food retail businesses globally.

Its SA Food business is unquestionably the best food retail business in South Africa, with a strong return on capital close to 70%. Its aspirational brand, unmatched product innovation and affluent customer base give it the pricing power to easily pass on input inflation, making it a very defensive consumer business. Food delivers 50% of WHL’s profit before tax, providing a solid underpin to group earnings.

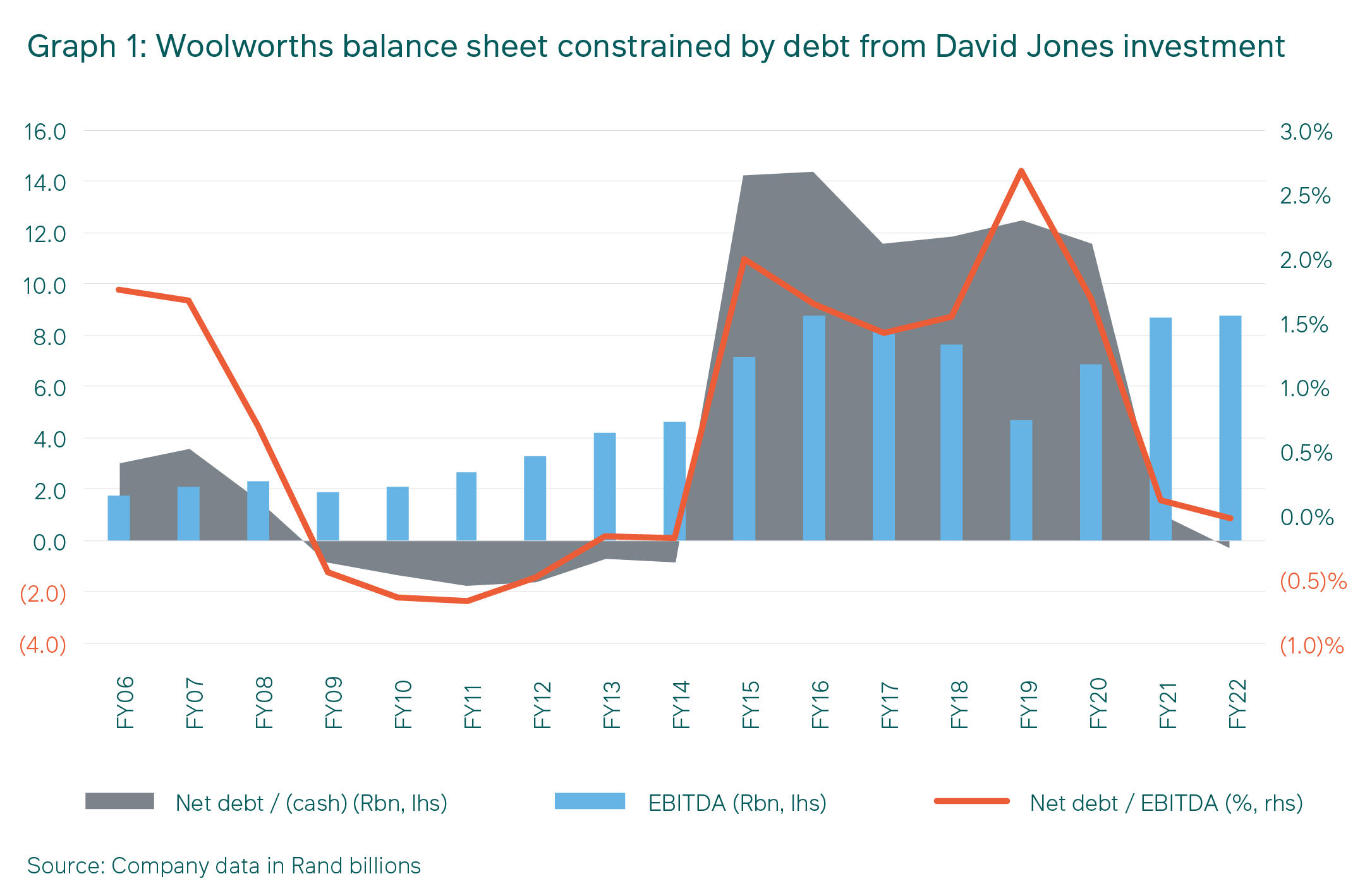

In the early 2010s, the highly cash-generative nature of the Food division enabled WHL’s balance sheet to be in a net cash position (see Graph1), while still funding dividends and growth (i.e., rolling out new stores and building the supply chain). However, this changed when WHL accelerated its strategy to be “A leading Southern Hemisphere Retailer” with the acquisition of Australia-based David Jones in 2014. This turned out to be a poor investment (we detail why below) and unfortunately also consumed WHL management’s attention at a time when the local Fashion, Beauty and Home (FBH) division was struggling in an increasingly competitive market.

Click chart to enlarge

Woolworths has been on a journey to fix the mistakes of previous management since Roy Bagattini took over as CEO in February 2020, and we think it is making good progress. The upside in the WHL investment case hinges on the company’s ability to continue executing the operational fix of the FBH division and to exit David Jones.

What went wrong

The two key drivers of Woolworth’s poor share price performance from 2015 onwards (see Graph 2) were the company’s FBH business in SA and David Jones in Australia. These businesses underperformed both in absolute terms (FBH profits declined from R2.1bn in FY2015 to R1.8bn in FY2019; DJ profits fell from R1.1bn to R0.3bn in 2FY019) and in relative terms.

Click chart to enlarge

Fashion, Beauty and Home

FBH was historically known as Clothing & General Merchandise (CGM), as Beauty only became a key focus area post the demise of Edcon, the retailer that dominated South Africa’s beauty category. The fashion sub-division of the FBH business has always targeted a slightly more mature, affluent consumer, who wants good-quality, conservative fashion. Historically they did this very well, but started to lose market share when the international apparel retailers expanded in SA from the early 2010s (i.e., Cotton On, Zara and H&M). To grow the business, WHL decided it needed to broaden the appeal of their offering by becoming more fashion-orientated and targeting a younger, less affluent consumer. Christo Claassen was appointed MD of FBH in mid-2014 to drive this strategy. WHL hoped his experience of running Jet (Edcon’s value brand) would assist them in successfully executing this strategy, as fashion and value were not their core competencies. Unfortunately, the opposite occurred.

To compete successfully in the mid-tier apparel category, a retailer needs to offer competitive price points and get fashion calls right consistently. New sub-brands (e.g., Edition) with a higher fashion focus were launched, but numerous fashion mistakes were made, which resulted in FBH having bigger and deeper sales to get rid of the stock, something that is very negative for profit margins.

In addition, to maintain gross profit margins at the lower price points, the quality of the product (e.g., material, buttons, zips, etc.) was lowered. This had a drastic impact on the brand’s reputation for quality and value, as often within a few washes a garment would lose both its shape and colour. The soles of a pair of shoes I bought for my toddler fell off the second time he wore them.

Post the acquisition of David Jones, WHL also chose to rebrand its core ranges from Woolworths, an iconic South African brand, to David Jones, a brand that the average South African didn’t know. Swapping from a strong brand to one that had no brand equity in the local market never made logical sense.

WHL acknowledged they had the wrong person leading FBH and removed Christo Classen in September 2018. Manie Maritz, highly respected in the apparel industry due to building Markhams into one of The Foschini Group’s most successful brands, was appointed, but frustratingly his non-compete clause meant he could only start at FBH in mid-2020. For over 18 months, FBH operated under a caretaker MD, and the lack of strategy was evident in the further deterioration of the operations.

The above resulted in FBH’s revenue growing by only 1.6% p.a. between FY2014 and FY2021 and profit margin declining from a peak above 19.0% in FY2014 (IFRS 16 adjusted) to 8.0% in FY2021.

David Jones

In 2014, WHL embarked on a strategy to build a leading Southern Hemisphere retailer by acquiring David Jones for R21bn (representing 32% of WHL’s market capitalisation at 9 Apr 2014). The David Jones department store model was very similar to the FBH model, and WHL had owned the Country Road Group in Australia for 15 years, hence they thought their knowledge of the market and business model mitigated the risk of doing such a sizeable acquisition.

Department stores have been around since the late 1700s, but gained their prominence in the mid-1900s. Their success emanated from the convenience and consumer experience they offered by housing multiple brands across many categories (apparel, footwear, beauty, home, etc.) in one beautifully designed store. A consumer could get everything they needed in one pleasant shopping environment. However, the establishment of discounters in the late 1900s eroded the value proposition of department stores, while the rise of e-commerce in the 2000s has usurped their convenience aspect. As a result, countless department store businesses have gone bust globally -- for example, Debenhams, a famous UK department store founded in 1778, closed in 2021.

While investors raised concerns about WHL acquiring a business that operated a shopping format that was declining globally, the opportunities to improve David Jones’s operating performance were significant.

Initially, good progress was made in improving inventory management; however, the strong force of declining demand for the department store format resulted in revenue not growing after FY2016. Poor execution of the David Jones private label strategy caused gross profit margins to decline from 40% in FY2015 to 35% in FY19. Combined with operational expense growth from implementing new IT systems, launching a loss-making premium food offering and rolling out more stores, this resulted in the operating profit margin declining from 15% in FY2015 to low single-digits in FY2021. These poor operational results necessitated WHL impairing R13bn (62% of the acquisition cost) of the David Jones value.

Ian Moir, the previous CEO of WHL, pushed David Jones into a strategy of premiumising its product offering and store formats, with the aim of creating the best department store in the world. To do so, WHL approved a capex budget of A$200m to renovate their flagship Sydney store and convinced the brands (suppliers) to also invest A$200m into their areas within the store. This created a spectacular store for customers, but shareholders are unlikely to ever see a positive return from this immense investment. To afford this, the Sydney menswear store was consolidated into the Elizabeth Street womenswear store and the menswear building sold for A$360m.

Investors became especially nervous about how David Jones was going to replicate this shopping experience across its 48 stores, not just because of the capital cost but also due to concerns on whether the affluence of its customer base was sufficient for such a premium product offering. Andrew Jennings, an ex-CEO of WHL/Harrods/Saks 5th Avenue (i.e., a premium department store expert), has stated this premium department store model would only work with fewer than 10 stores. With an average remaining lease term of 15 years, David Jones is unable to implement Jennings’s advice of exiting the bulk of their stores quickly.

The poor operational performance forced WHL to stop extracting dividends from the Australian operations, as cash was needed to fund the significant capex. Increased debt funding was required, as the internal cash generation was insufficient, and WHL had (rightly) made the call to stop providing funding from the SA operations. The increasing probability of WHL being forced to inject more capital from SA into David Jones weighed heavily on the WHL share price, as seen in Graph 2.

Fixing the underperforming divisions

The positive changes initially started in FY2019, when five new Board members were appointed. The two most significant changes were the appointment of David Kneale, the very highly rated ex-Clicks CEO who brought in substantial retail experience, and the appointment of Hubert Brody as Chairman, who was truly independent. In January 2020, Roy Bagattini was appointed as CEO of WHL, while the architect of the strategy which led to the demise of FBH and David Jones, Ian Moir, was demoted from Group CEO to David Jones CEO. The market questioned Bagattini’s appointment, as his previous role as MD of the America’s division of Levi Strauss & Co positioned him well to run the pure fashion business (i.e., Country Road Group), but he had limited to no experience in running a food retail business (WHL Food) or department stores (FBH and David Jones).

Turning around a business is a difficult task; doing so during a global pandemic is exponentially harder. Just over two-and-a-half years into the role of CEO, Bagattini is starting to gain the trust of the market as the initiatives he has implemented are bearing fruit.

Within FBH, Bagattini and Maritz have made the following changes:

- Rationalised space by 13%, with another 3% to be cut in 2022 – exited loss making space;

- Narrowed the range (discontinued 2 sub-brands) – improving procurement efficiencies;

- Improved customer segmentation, focused on must-win categories, the categories where WHL was historically very strong and improved the product quality (back to the quality a WHL customer expects);

- Enhancing the Beauty and Home offerings – attempting to become the market leader in these categories that were previously dominated by Edgars;

- Increasing local procurement - enables them to react faster during a season to take advantage of the best-performing trends;

- Leveraging customer data better, in an attempt to convert the incredibly strong brand loyalty of the Food division customer into an FBH customer; and

- Optimising the supply chain, which remains the biggest opportunity for FBH, since a frequent customer complaint is FBH not having the customer’s size. This implies WHL is getting the fashion call right (the customer wants to buy the product).

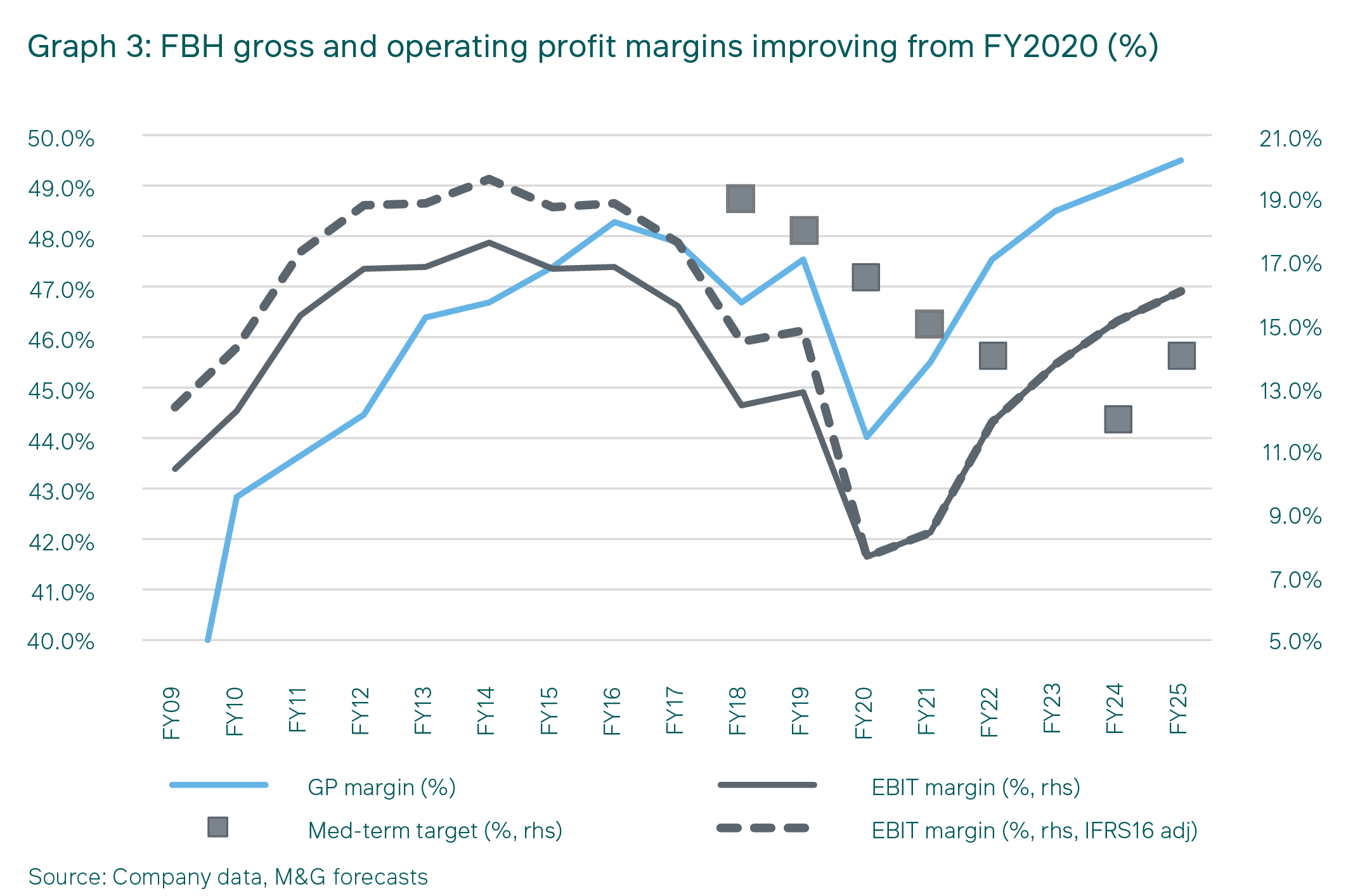

While a number of these initiatives are only in the very early stages, they have had a material impact on the operational results of FBH already, with FY2022 sales only 4.8% lower than FY2019 despite the 13% reduction in space. Full-price sales are growing materially faster than total sales, which has reduced the markdown ratio (markdowns as a % of total sales) from 20% in FY2020 to 13% in FY2022 and lifted the gross profit margin in 2H2022 to 49%, the highest level in a decade.

This, combined with good control of operational expenses, has led to the operating margin improving to 11.9% from the Covid low of 7.6%. Importantly, WHL felt comfortable enough to raise the medium-term operating profit margin target from 12% to over 14%. We think WHL is still being too conservative with their operating margin guidance, as management stated there is no reason why their markdown level should not be in line with the global average of 10% (i.e., 3% better than the current 13%). This further 3% improvement should flow through to the bottom line. Graph 3 indicates how conservative the 14% margin target is.

Click chart to enlarge

Bagattini’s core focus with respect to David Jones was separating the legal entities of the two Australian businesses. Country Road Group (CRG) had cross-guaranteed the other company’s debt, which constrained WHL from closing David Jones, as the debt would need to be serviced by CRG. To reduce the debt to a level at which the banks were comfortable renegotiating the terms (i.e., removing the cross-guarantee) required selling two of David Jones retail properties for a combined A$631m (Bourke Street in July 2020 for A$121m and Elizabeth Street in March 2021 for A$510m). These sales enabled all the Australian debt to be repaid and put both David Jones and CRG in net cash positions. Importantly, WHL is now in a position to sell David Jones without having any impact on CRG, and CRG can focus on growing their own business.

The operational fixes within David Jones have included the launch of a loyalty card to improve value offered to customers, reducing space by 10%, with another 8% reduction planned by 2024, improving the private label offering to increase differentiation, launching online (now 20% of sales) and discontinuing the loss-making food strategy. These actions resulted in the operating margin improving to 4% in FY2022 from a loss in FY2020, but this remains well below the mid-teen margins of FY2015/2016 (on an IFRS16 adjusted basis). As a result of the reduced capex and operational fixes, cash flow generation has improved to a point where WHL has been able to extract dividends of A$90m in FY2022 and a further A$50m in FY2023, which have been used to pay down debt at the WHL Group level and return the Group net debt to pre-David Jones acquisition levels of 1.6X net debt to EBITDA.

Although the sustainability of the David Jones operational improvement remains questionable, we are increasingly confident that WHL will be able to sell the business for a reasonable sum. Firstly, it still owns one store (310 Bourke Street, Melbourne) which, based on the sale of 299 Bourke Street in July 2020, should be worth approximately A$218m. The company also has at least A$40m excess cash, after accounting for the A$50m special dividend (noted above) and 1H2023 working capital needs, and the business is generating cash. In addition, Myer, David Jones’s closest competitor in Australia, has a market cap of A$460m. David Jones deserves to trade at a discount to Myer, given its relative operational underperformance, but we don’t think this discount should exceed 30%, implying a potential David Jones’s market cap of A$320m. Therefore, at worst WHL could extract A$260m (or R3 per WHL share) by selling the Bourke Street property and repatriating the excess cash, with another A$320m (R7 per WHL share) potentially achievable if they find a buyer for David Jones.

Outlook

In our view, the challenges of David Jones are largely behind WHL, and the group balance sheet is now in a far healthier position, enabling WHL to focus on continuing the operational fix of the FBH division and to refocus on investing in growing its higher-quality Food and Country Road divisions. Although the consumer is likely to come under increasing pressure over the next year, we are confident that WHL has sufficient self-help levers-- and is using them -- to outperform the other retailers in difficult economic conditions, with upside optionality if they do exit David Jones.

At the same time, we were able to buy WHL shares for our client portfolios at a cheap valuation compared to both their history and our estimate of fair value. For these reasons, we expect our WHL holdings to add value to our clients’ portfolios over the medium term.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter