South Africa

South Africa Namibia

Namibia

Chris Wood

Senior Portfolio Manager

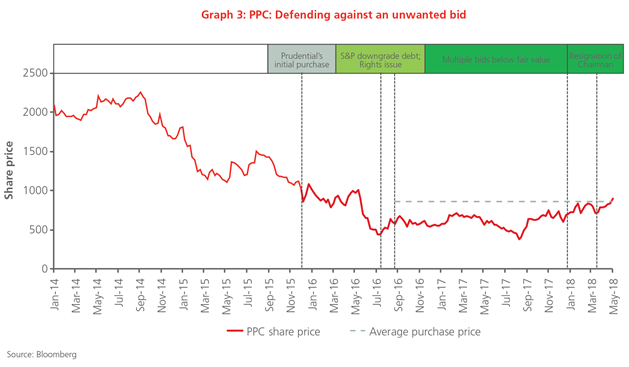

Shareholder activism (4): PPC: Defending against an unwanted bid

In the face of Steinhoff and other cases of shareholder value destruction in the past year, we've heard much debate around the effectiveness of shareholder activism. Prudential strongly believes in being an active and engaged shareholder to both protect and unlock value in our clients’ investments. In this article, the last in our series of four articles on shareholder activism, Prudential Senior Portfolio Manager Chris Wood shares an example of this – our opposition to the takeover attempts of cement producer PPC by local and international rivals.

PPC is a case in which we fought against several hostile takeover offers that we believed materially undervalued the company and would have left our clients with lower returns than otherwise possible. The graph below depicts our shareholder journey with PPC.

We bought an initial shareholding in the company in December 2015 at around R10.00 per share, after its share price had more than halved in value over the preceding two years. At the time the South African cement industry’s profitability was suffering from a combination of overcapacity, brought on by new entrants Sephaku and Mamba Cement, as well as weak market demand stemming from slow economic growth. However, with PPC nearing the completion of four new cement projects in Africa, we were expecting a turnaround in its future cash flows. By mid-2106, this ambitious African growth strategy had taken its toll on PPC’s balance sheet, prompting S&P Global Ratings to downgrade its debt, which in turn triggered an early redemption of its R1.9 billion outstanding corporate bond. PPC did not have the ability to repay its bond holders and was forced to raise capital through a deeply discounted rights issue at R4.75 per share. Prudential took up additional rights such that we ended up holding 15% of the company (on behalf of our clients), making us PPC’s second-largest shareholder.

In early 2017, PPC entered friendly merger discussions with rival cement producer AfriSam, but these negotiations failed. Subsequently, AfriSam teamed up with Canadian investment firm Fairfax to launch a hostile bid, which in turn led to other global cement competitors (including Irish group CRH, Lafarge ,one of the largest cement producers globally and in Africa, and Dangote Cement of Nigeria) entering the bidding fray. In our opinion, these were all very opportunistic offers, coming at a point where PPC’s profitability was depressed and its market rating low. We believed the bids significantly undervalued the company’s existing business, and failed to attribute value to the longer-term potential of its expanding African operations. PPC had also restructured its South African business, and was expecting improved profit margins in the local market. In fact, we were forecasting that PPC’s operating profit and associated cash flow would nearly double over the next three years.

Although the AfriSam/Fairfax offer of R5.75 per share was higher than the rights offer price – and therefore offered shareholders the opportunity to bank a short-term gain – we believed it risked transferring significant future value to the bidding consortium. We felt strongly that the best longer-term outcome for shareholders was for PPC to remain an independently listed company, so that investors could benefit from the material uplift in profits expected from its four new African plants ramping up production. Consequently, we wrote letters to the PPC Board of Directors outlining our opposition to all of the bids, and had numerous engagements with company management and other shareholders. The Board ultimately reached the same conclusion, and in December 2017 terminated discussions with all interested parties.

Subsequently, Prudential, together with the support of other large shareholders the Public Investment Corporation (PIC) and Value Capital Partners, moved to restructure the Board, replacing the Chairman and adding new non-executive directors that brought improved skills and expertise to the group. We felt these changes were necessary to give the company a strong platform for further long-term growth.

Today we remain a significant shareholder in PPC and are confident in our decision to fend off the opportunistic takeover attempts.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter