South Africa

South Africa Namibia

Namibia

Chris Wood

Senior Portfolio Manager

Shareholder activism (1): Red-flagging Steinhoff’s business model

In the face of Steinhoff and other high-profile cases of shareholder value destruction in South Africa in the past year, we've heard much debate around the effectiveness of shareholder activism. Prudential strongly believes in being an active and engaged shareholder to both protect and unlock value in our clients’ investments. In this article, the first in our series of four articles on shareholder activism, Prudential’s Senior Portfolio Manager Chris Wood shares an excellent example of how this works – our refusal to invest in Steinhoff due largely to its opaque business model.

In accordance with our responsibility as a custodian of our clients’ savings, if we disagree with the way a company is being managed, or if the business model is opaque or financial disclosure inadequate to allow a comprehensive understanding of the operations, we must be vocal and engage directly with management and other stakeholders.

Most investors will be familiar with Steinhoff, whose management shocked the market in December 2017 with the announcement of the resignation of its CEO, Markus Jooste, and the acknowledgment that its financial statements could not be relied upon due to allegations of accounting irregularities dating back several years. While many of these allegations are yet to be substantiated, evidence against senior management has continued to mount, leading to a devastating collapse in the Steinhoff share price in the ensuing months.

Prudential has maintained a high-profile negative view on Steinhoff since the early 2000’s. Among our many concerns were:

- The company’s weak balance sheet;

- Poor quality earnings that did not translate to cash flow, and consequently very low cash dividends paid to shareholders;

- A very low (often negative) value of tangible assets, while intangible asset value (attributable to more opaque assets like the brands it acquired) made up a very large and rising proportion of its net asset value;

- An extraordinarily low tax rate; and

- A highly acquisitive strategy funded with the excessive use of low-cost debt and continual issuance of new shares.

Following its acquisition of the highly cash-generative Pepkor business in 2014, Steinhoff’s weighting in South Africa’s equity market indices increased materially. At its peak, Steinhoff comprised over 4.5% of the JSE SWIX All Share Index. The potential for improved cash generation following the Pepkor acquisition, plus the active risk limits that Prudential imposes in managing our funds, led us to adopt a marginally less negative view on Steinhoff. From having historically avoided Steinhoff, Prudential accumulated a relatively small position – although we retained a significant underweight exposure. Steinhoff's 5 December 2017 announcement gave support to our initial concerns around Steinhoff, along with profoundly negative implications for the future of the company as a going concern. We immediately sold all our Steinhoff shares on that day, which has materially limited losses for our clients.

During the many years in which Prudential took an active decision to avoid Steinhoff or to hold a large underweight position, we were constantly challenged for our negative view, particularly during periods when Steinhoff was a meaningful detractor from our portfolios’ performance. However, in the end our consistent view and active stance paid off: clients have benefited from our conscious decision to exclude Steinhoff.

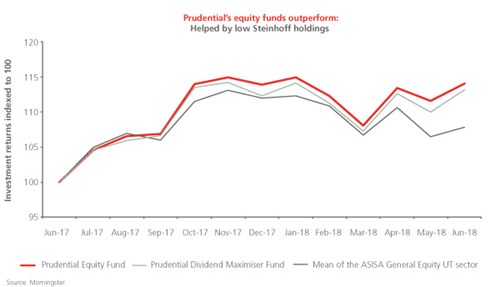

(CLICK ON GRAPH TO ZOOM)

The image illustrates the cumulative outperformance of our equity funds over the past year partly as a result of our Steinhoff view. For the 12 months ending 30 June 2018, both the Prudential Equity Fund and Prudential Dividend Maximiser Fund have substantially outperformed the mean return of the ASISA General Equity unit trust category, with the single largest contributor to this outperformance being the funds’ underweight exposure to Steinhoff. The Prudential Equity Fund has returned 14.1%, an outperformance of 6.2% for the 12 months net of fees, while the Prudential Dividend Maximiser Fund has returned 13.2%, 5.3% above the mean peer fund.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter