South Africa

South Africa Namibia

Namibia

Aeysha Samsodien

Portfolio Manager

Mining: a key component in the just energy transition

It’s no secret that South Africa’s mining industry faces significant challenges, such as energy reliability, environmental impact, supply chain problems, and policy uncertainty, to name a few.

At the same time, we believe that an opportunity exists in this sector: the just energy transition.

Mining’s contribution to South Africa’s GDP peaked in the 1980s at about 20%. Currently, it only contributed 7.5% of GDP, or around R500 billion; a substantial contraction at the end of 2022.

Nevertheless, mining remains an important contributor to the fiscus having paid some R73 billion in company tax last year (21% of total company tax) and royalties of R14.2 billion (levies paid for extracting natural resources). However, we anticipate that the revenue collected going forward will decline because of the falling commodity prices, particularly in Platinum Group Metals (PGM). The sector is also a large employer with just under half a million jobs provided, or 4.8% of total jobs, which doesn’t include the indirect employment, through the various supply chains linked to the industry.

The mining sector accounts for roughly a third of the JSE’s market capitalisation and is a highly cyclical and volatile sector. In addition, there are companies, such as BHP Billiton that remain listed on the exchange even though they no longer have operations in SA or contribute to local GDP.

What influences global mining?

Global growth expectations are a driver of the mining industry as it impacts the demand for commodities. When a country is growing it spends on infrastructure, which drives the consumption of commodities. Once infrastructure is in place, economies switch to a focus on manufacturing consumer products, such as home goods, phones, even jewellery - all of which require commodities. But the relationship between GDP and commodities is interconnected. This played out in 2022 when the Russia-Ukraine war started, exacerbating supply chain disruptions. The underinvestment in energy drove the prices to elevated levels, which led to higher inflation and global recession concerns.

China has been one of the integral drivers of commodity markets over the last 20 years with its focus on industrialisation and urbanisation. While the Chinese economy has slowed in recent years, it still consumes approximately 50% of global commodities, including iron ore, aluminum, copper, nickel, and zinc. China hasn’t yet reached its urbanisation goals of 65% (currently at 60%) and so their infrastructure spend is expected to continue in the short to medium term, however, China’s property market crisis remains a concern in the short term.

The next commodities boom: clean energy

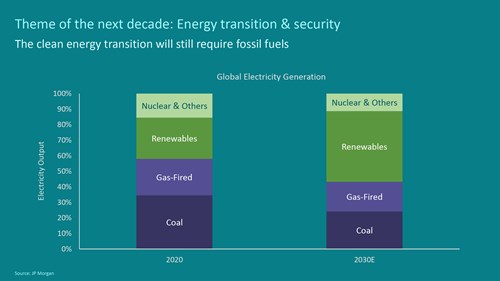

Currently coal and gas, which are fossil fuels, account for just over 50% of global energy generation, while renewables stand at 20-25%. To meet our aspirations to mitigate climate change, we need to increase the use of renewables. As a result, the need for renewable energy will increase significantly over the coming decades.

However, as economies also need energy security, fossil fuels will still be a key part of the energy mix and investment in fossil fuels will continue (as seen in the chart). There is also a need to ensure that the energy transition is affordable for all countries as we are taking this journey together.

From the chart, it’s evident that commodities play an integral role in the energy transition. However, due to underinvestment in supply over the last decade, there are supply constraints in the energy transition journey. By way of example, to acquire enough copper for the energy transition we need to mine more than has ever been mined before. To put this energy transition demand for copper into context, we would need to build 300-400 mines globally over the next 10-15 years. But in order to achieve a just energy transition, we need to strike the balance between meeting current demand for commodities required in consumers’ everyday lives with the increased demand going forward for the energy transition journey. In addition, increasing demand too swiftly to meet both current and future needs must be done carefully to manage the risk of price increases that could damage economic growth.

However, the South African mining sector is coming to the party and committing to renewable energy both to reach their net zero aspirations as well as improve energy security against the constraint of energy availability. To this date, company announced installed capacity is under 1000MW but there are significant plans to increase that to over 6000MW over the next decade, but the process is largely dependent on electricity grid capacity. Over the last few months, we’ve seen company announcements coming through on increasing planned capacity over the next few months and years. The mining sector accounts for about 50% of the planned announcements, which will help with energy security, transition and hopefully costs as well. The mining sector is meaningfully stepping up to the plate.

The mining sector influences and is influenced by various macro and local dynamics, such as the global economic growth outlook, China’s commodity consumption, and homegrown challenges, like energy constraints, railway infrastructure challenges, etc. One of the ways we believe these local challenges can be addressed is through public-private partnerships. However, the just energy transition presents an opportunity for mining both locally and globally.

When building portfolios and looking at the markets, we carefully consider the risks and evaluate the opportunities. While faced with enormous challenges, the mining sector is a significant contributor to local economic growth, and looking ahead, will be critical in the energy transition. Mining sector positions in our M&G Equity and Dividend Maximiser Funds have contributed to alpha on an absolute and relative basis over the past 20 years, and we believe it is worth holding consistently as the next commodities boom unfolds.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter