South Africa

South Africa Namibia

Namibia

Sandile Malinga

CIO Multi-Asset

Market Observations: Q4 2023

The final quarter of 2023 saw a synchronized rally across global bonds and equities as falling inflation in many economies led central banks to continue to pause or effectively end their interest rate hiking cycles and start to look towards rate cuts, particularly in the US. And, although a growth slowdown is still expected in 2024, this and the gradually improving outlook buoyed investor sentiment, resulting in strong gains in November and renewed bullishness in December, to end the year with unexpectedly good asset performance.

December’s returns were dominated by the US Federal Reserve’s unexpectedly positive forecasts at their 13 December policy meeting as, besides leaving interest rates on hold, they clearly indicated their expectations for three 25bp interest rate cuts in 2024, as well as forecasting a “soft landing” for the US economy. They also added that they didn’t want to make an error by “waiting too long” to begin lowering rates. This was very good news for both equity and bond markets, helping bolster the 2024 outlook despite the uncertainty still surrounding the cumulative negative impact from the steep rate hiking cycle. Other large central banks also left interest rates on hold at their December policy meetings as expected.

Global equity (as measured by the MSCI ACWI) delivered 11.0% in Q4, emerging market equities returned 7.9% (MSCI Emerging Markets Index) and global bonds produced 8.1% (Bloomberg Global Aggregate Bond Index, both in US$). In South Africa, the FTSE/JSE Capped SWIX Index posted an 8.2% return in rand and somewhat stronger than other emerging markets. Gains were propelled by a strong 15.9% rebound in the All Property Index over the quarter and 11.8% from Financials, while Industrials delivered 5.9% (hit by a sharp fall in Naspers/Prosus shares in December) and Resources stocks were flat (0%). South African bonds delivered an impressive 8.1% for the quarter. This saw the yield on the 10-year SA government bond tumble from just over 11% at the start of the quarter to 9.8% by the end. Meanwhile, the rand gained 2.7% against a weaker US dollar in Q4, but in total lost 8.2% against the US dollar, 14.1% versus the UK pound and 12.1% against the euro in 2023.

For 2023 as a whole, global equities returned an excellent 22.2% in US$ and 32.3% in rand (due to rand depreciation), with gains fairly concentrated around a handful of giant global AI-related US companies, termed the “magnificent seven”: Apple, (up 54%), Amazon (up 77%), Alphabet (up 57%), Nvidia (up 246%), Meta (up 184%), Microsoft (up 57%) and Tesla (up 130%). These outpaced other US shares and, indeed, most other equity markets for the year, making the US meaningfully more expensive than its global counterparts. This also reflected the relative vitality of the US economy versus most other large economies. By contrast, Chinese tech stocks were deep in the red, with Tencent losing 54% for the year, Meituan -54%, JD.com -50% and Welbo Corp -44%.

Global bonds experienced a very volatile year, marked by rapid shifts in the interest rate outlook and investor sentiment that pushed the yield on the benchmark 10-year US treasury bond to 5% (briefly) in October and left it trading around 3.8% at year-end, presenting opportunities for active investors to harness attractive above-inflation yields. Ultimately, global bonds as an asset class returned 5.7% for the year.

South African assets were weighed down in 2023 by ongoing general pessimism over the country’s weak growth prospects, loadshedding and uncertain government finances, exacerbated by the higher risks associated with the grey-listing of SA in global financial transactions and incidents like the “Lady R” and hosting of the BRICS Summit. This manifested in rand weakness, equity underperformance against the MSCI EM Index and continuing low valuations on SA stocks and bonds. The FTSE/JSE ALSI returned 9.3% and the more domestically-focused FTSE/JSE Capped SWIX Index posted 7.9% for the year. However, SA bonds notably outperformed their global counterparts for the year, helped by their cheap valuations at the start of 2023, delivering a 9.7% annual return.

|

Asset class |

Total return Q4 2023 (Rand and US$) |

Total annual return 2023 (Rand and US$) |

|

SA equity – FTSE/JSE All Share Index (Rand) |

6.9% |

9.3% |

|

SA equity – FTSE/JSE Capped SWIX All Share (Rand) |

8.2% |

7.9% |

|

SA listed property – FTSE/JSE All Property Index (Rand) |

15.9% |

10.7% |

|

SA bonds – FTSE/JSE All Bond Index (Rand) |

8.1% |

9.7% |

|

SA inflation-linked bonds – FTSE/JSE Composite ILB Index (Rand) |

6.1% |

7.1% |

|

SA cash - STeFI Composite Index (Rand) |

2.1% |

8.1% |

|

Global equity – MSCI All Country World (Total, US$ net) |

11.0% |

22.2% |

|

Global equity – MSCI World (Developed) (US$ net) |

11.4% |

23.8% |

|

Global equity – MSCI Emerging Markets (US$ net) |

7.9% |

9.8% |

|

Global bonds – Bloomberg Global Agg Bond Index (US$ net) |

8.1% |

5.7% |

|

Global property – FTSE EPRA/NAREIT Global REIT Index (US$ net) |

15.2% |

9.6% |

Source: M&G Investments, Bloomberg, data to 31 December 2023

United States

In the US, the Fed’s December forecasts for 2024 showed inflation falling gradually toward its 2% target amid a slowdown in growth, without steep job losses. Unemployment is seen rising to 4.1% from its current 3.7% level, still low from a historic perspective, and GDP growth is forecast to average 1.3% for the year. Meanwhile, at 3.1% y/y, November CPI was in line with expectations and down from October’s 3.2% y/y, helped by lower energy prices over the period. For the quarter, the Dow Jones produced 11.7%, the Nasdaq 13.1%, and the S&P 500 13.8% (all in US$). The Nasdaq was the top-performing developed equity market in 2023 with a remarkable return of 44.6%.

UK

In the UK, the Bank of England (BoE) kept its main interest rate unchanged at 5.25% at its December meeting, saying its next move would remain data-dependent, but the market is pricing in the start of rate cuts from June 2024. November CPI fell sharply to 3.9% y/y from 4.6% in October. The UK economy is on the verge of recession, having recorded zero (0%) GDP growth in Q3 2023, and with the BoE downgrading its growth forecast for 2024 to 0% from 0.5% previously. For Q4 2023, the FTSE 100 returned 14.4% in US$ and for the 12 months it produced 14.4%.

Eurozone

In the eurozone, inflation continued to fall during the quarter, with the latest November CPI at 2.4% y/y% nearing the ECB’s 2% target rate. However, the central bank’s latest forecasts show inflation improving only very slowly going forward and averaging 2.7% in 2024 from 5.3% in July. GDP growth in the area registered a paltry 0.1% y/y in Q3 2023, and is expected to remain very subdued at 0.8% y/y in 2024. While leaving interest rates unchanged at is 14 December policy meeting, in contrast to the Fed, the ECB remained hawkish, continuing to warn of upside inflation risks from energy prices and labour costs, and discounting the possibility of interest rate cuts in the foreseeable future. In European equity markets, France’s CAC 40 returned 10.5% in Q4 and 24.4% for 2023 as a whole, while Germany’s DAX delivered 13.6% in Q4 and 24.5% for the year (all in US%).

Japan

After impressive growth in the first half of the year, Japanese GPD shrank by a more-than-expected 2.9% in Q3 2023 (annualised, revised) as consumer and business spending contracted and real wages fell due to prolonged relatively high inflationary conditions. The sharp slowdown came despite the Bank of Japan maintaining its ultra-easy monetary policy, which had provided firm support previously and also helped push the local equity market to 33-year highs in December. The latest conditions suggested that the BOJ will continue to keep interest rates exceptionally low, in line with the central bank’s goal of keeping inflation sustained at around 2% and avoiding deflationary conditions. The Nikkei returned 11.4% (in US$) for Q4, and 22.6% in 2023.

China

During the three months, the Chinese economy gained traction with Q3 GDP growth reported at a stronger-than-expected 4.9% y/y (vs 4.4% y/y forecast). Although this means that the government is likely to meet its 5% GDP growth target for 2023, the absolute level of growth has continued to disappoint. The country’s exports remained under pressure from relatively weaker foreign demand, but looser monetary policy from the People’s Bank of China (PBOC) has added stimulus through lower bank rates for its medium-term lending facilities. There was positive news with November data showing industrial production grew faster than expected at 6.6% y/y (versus 5.6%), up from 4.6% y/y in October, and retail sales growth of 10.1% also improving significantly from 7.6% the previous month. Pent-up consumer demand continues to underpin the expansion, along with consumer services, while the property sector remains in crisis and youth unemployment high. After posting a weak equity performance for much of the year, Chinese markets were still fairly weak in Q4, with Hong Kong’s Hang Seng returning -3.7% and the MSCI China delivering -4.2%, both in US$. For the year, the Hang Seng produced -10.6% and the MSCI China posted -11.0%

Emerging markets

With the exceptions of China and Turkey, larger emerging equity markets performed very strongly over the quarter. Brazil’s Bovespa soared with a return of 18.6%, followed by South Korea’s KOSPI with 13.9%, the MSCI South Africa at 12.7% and the MSCI India at 12.0% (all in US$). The MSCI Turkey fell 12.1% (both in US$).

Commodities

Global inflationary pressures eased somewhat in Q4 as the international oil price fell 19.2% during the period amid concerns over increasing global crude supplies (largely from non-OPEC+ producers) and slowing demand. Brent crude was trading at around US$93/bbl at the beginning of October, but ended December at around US$77/bbl. For 2023 as a whole, the oil price fell approximately 10%. Other commodity prices were mixed amid the uncertain outlook. Among precious metals, gold gained 13.1%, while platinum rose 9.1% and palladium dropped 11.7%. Nickel was the largest loser, down 11.9%, while aluminium gained 1.2%, copper was up 3.0% and zinc was flat. In 2023 as a whole, nickel experienced a sharp 46.4% fall, as did palladium at 38.7%, while platinum, zinc and lead were down 8.0%, 12.7% and 13.0%, respectively. Gold was the strongest performer with a 13.1% price gain in 2023.

South Africa

In South Africa, at its 23 November policy meeting the SA Reserve Bank voted unanimously to keep the repo rate steady at 8.25%, as expected. Governor Lesetja Kanyago still sounded relatively hawkish regarding inflation, but noted that growth was likely to remain muted due to ongoing energy and logistical constraints (at ports and railways) weighing on economic activity and adding to the costs of doing business. Q3 2023 GDP failed to grow, contracting more than expected at -0.7% y/y (versus -0.2% forecast), with output declining in agriculture, mining and construction, while services output expanded. Looking ahead, the SARB projected GDP growth at 0.8% for 2023, 1.2% in 2024 and 1.3% in 2025, the latter improvements due largely to added electricity supply. Besides local headwinds to growth, China’s ongoing slower growth presents challenges for SA’s commodity exports.

Headline November CPI declined to 5.5% y/y from 5.9% y/y in October, largely on the back of energy price decreases. However, after falling in Q3, surveyed inflation expectations for 2024 rose to 5.7% from 5.5% in Q3, according to the BER. Consumer confidence remained in the doldrums, as the FNB/BER Consumer Confidence Index registered -17 points in Q4 from -16 points in Q3.

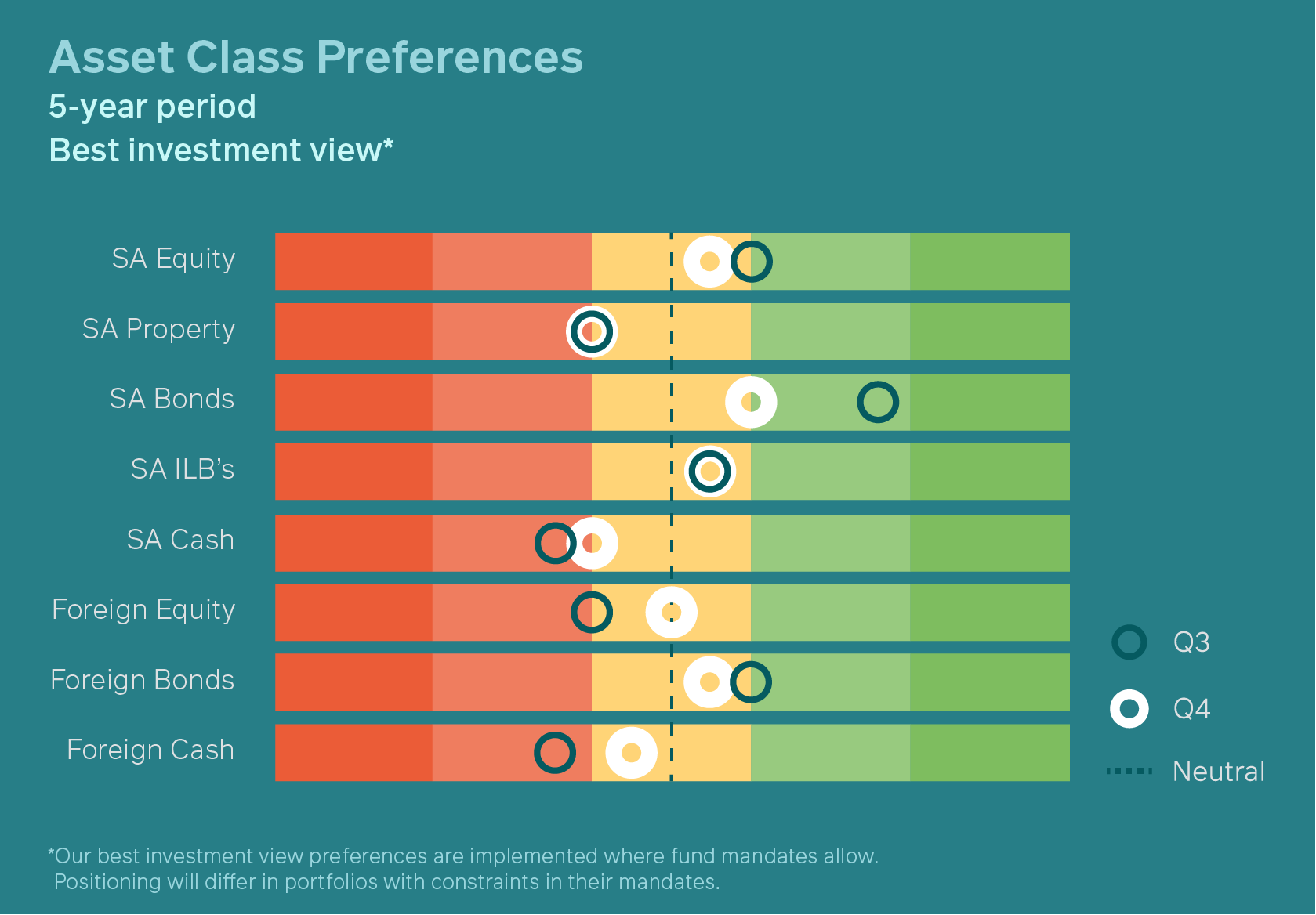

How have our views and portfolio positioning changed in Q4 2023?

Starting with our view on offshore vs local asset allocation in our house-view portfolios, during the quarter we increased our offshore exposure and reduced our total SA exposure: we trimmed our SA assets across equity, listed property and bonds and used the proceeds to buy global equities and increase our cash holdings. However, we continued to prefer more attractively valued SA assets compared to their global counterparts.

Within our global holdings, during Q4 we bought more global equity out of our SA holdings, so that our position moved from slightly underweight to slightly overweight at quarter-end as the global growth outlook improved. Following the strong November rally in global bonds, we also took profits on a portion of our 30-year global bond exposure so that our portfolios moved from slightly overweight to slightly underweight, and duration also fell from modestly over- to underweight at quarter-end.

In global equities, the MSCI ACWI 12-month forward P/E rose to 16.8X at quarter-end from 15.9X at the beginning of the quarter as stock prices gained ground. We increased our weighting on the back of the modest improvement in the interest rate outlook; however, we remain concerned that US equities remained priced for a perfect “soft landing” outcome in 2024. As such we have moved only modestly overweight from our previously slightly underweight exposure, and remained tilted away from the relatively more expensive US market. Equity markets that we prefer for their cheaper valuations include the UK, Japan, China and other emerging markets.

Within global bonds, November’s sharp rally offered an opportunity for us to take profits on our holdings of 30-year US Treasuries, UK gilts and German bunds, thus reducing our overweight position in global bonds. Portfolio duration also fell. We used the proceeds to buy global equity and increase our global cash position. We continue holding moderate levels of local currency sovereign EM bonds where the real yields are high and the currency is trading at fair-to-cheap levels.

Our house-view portfolios were underweight global corporate credit at quarter-end, based on our view of credit spreads as unattractive for the risk involved versus their government counterparts.

Our house-view funds still favoured SA equities at the end of Q4 2023, although we did take some risk off the table by selling into the quarter’s rally and using the proceeds to buy global equities and increase our SA cash holdings. SA equity valuations (as measured by the 12-month forward Price/Earnings ratio of the FTSE/JSE Capped SWIX Index) rose to 10.0X from 9.5X at the beginning of the quarter. Local equity market conditions during the year favoured stock picking, given the wide dispersion in valuations across the market, and even within sectors. Some of the top stock holdings that made the most meaningful contributions to M&G Investments’ portfolio performance over the past 12 months included Textainer, Standard Bank, Investec and Richemont.

Global shipping container lessor Textainer has been a preferred holding for several years, having benefited significantly from the recovery in global trade following the Covid pandemic. It possessed a sufficiently strong balance sheet that enabled the company to participate in the trade recovery post covid and increase its container fleet substantially. As an early mover, the company took advantage of the extended container shortages due to the dislocations in global trade to lease out the acquired containers at favourable lease rates for longer lease durations. This was financed with fixed rate debt that helped it withstand the higher interest rate environment. In the slowdown, the management team demonstrated discipline, not pursuing market share at all costs and rather focusing on share buybacks and shareholder returns. In October this year, the group announced an all cash buyout offer by US alternative investment firm Stonepeak at a 46% premium to its share price, sparking equivalent share price gains in Textainer and adding excellent value to our client portfolios.

Standard Bank and Investec: M&G house-view portfolios have been overweight SA banks for some time, recognising that they are among the only businesses to benefit from rising interest rates as they receive more income from debtors and government bond holdings. There is a risk that debtors may default as interest rates rise, but at M&G we recognised that SA banks had been conservative in their lending practices in the run-up to, and during, the Covid pandemic, and had over-provided for bad debt in the economic downturn resulting from Covid, as well as in the conversion to a new accounting standard (IFRS 9). They had also had to comply with stricter lending regulations post the introduction of the National Credit Act in the late 2000s, giving them very healthy balance sheets at the beginning of 2023. Yet their valuations reflected the prevailing high uncertainty around inflation, interest rates and growth in SA and globally. Sentiment deteriorated further during the second quarter of the year after the emergence of the US regional banking crisis and rescue of Swiss banking giant Credit Suisse. Yet the banks consistently reported stronger-than-expected earnings and profits, successfully weathering the poor local conditions and helping lift their share prices. Among our bank holdings, Standard Bank and Investec added the most value to our portfolios over the period.

Richemont, the global luxury goods group, has been another large contributor to our portfolios’ performance in 2023 due to our active overweight in the stock. Despite its cyclicality, Richemont is a high-quality company with a regionally diversified business and a strong balance sheet reflecting a net cash position. The group also has strong free cash flows and a very strong balance sheet, being in a large net cash position. Richemont’s jewellery businesses experienced surprisingly strong sales growth throughout 2023 across all its brands like Cartier, Van Cleef & Arpels and Piaget, reporting record operating profit for its 2023 financial year ending 30 March. And this despite headwinds that were supposed to materialise because of economic slowdowns in China and the West. The company’s’ geographical diversification helped meaningfully as the robustness of the US economy (and Europe to a lesser extent) compensated for the slower-than-expected Chinese economic recovery post their COVID lock-down.

In Q4 we further lowered our already-underweight exposure in SA listed property by selling into that sector’s good performance, while buying global equity and lifting our cash exposure. Property sector risks remained high relative to other sectors, while cash yields have become more attractive. We still prefer exposure to non-property shares that we believe offer better value propositions for less risk. Conditions in the local property sector remain uncertain and growth prospects relatively weak, and many property companies are reliant on finance to expand their portfolios, among other fundamental factors.

We also sold some of our overweight holdings in SA nominal bonds, taking profit into the rally over the period. Still, we maintained our significant preference for these assets in our house-view portfolios. From a yield of over 12% at the start of the quarter, the 10-year SA government bond rallied by over 100bps to close the quarter at a yield of around 11%. We continue to believe SA nominal bond valuations are attractive relative to other fixed income assets and to their own longer-term history, and will more than compensate investors for their associated risks over time.

Although our house-view portfolios have no meaningful exposure to SA inflation-linked bonds (ILBs), we hold them in our real return portfolios such as the M&G Inflation Plus Fund. We did not make any adjustments to our ILB positioning during Q4, continuing to marginally favour these assets. Their real yields remain relatively attractive (compared to their own history and to our long-run fair value assumption), but their valuations are less attractive than nominal bonds, giving them lower return potential. We also prefer to add value to client portfolios by taking advantage of the changing interest rate outlook reflected in nominal bonds.

Lastly, we added to our SA cash holdings during the quarter after trimming some of our other SA exposure, but given our very underweight positioning prior to this, our portfolios remained tilted away from SA cash at quarter-end. Yields on cash-type instruments have become more attractive for investors following the SARB’s steep interest rate hikes in 2023.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter