South Africa

South Africa Namibia

Namibia

David Knee

Chief Investment Officer

Market Observations: Q2 2022

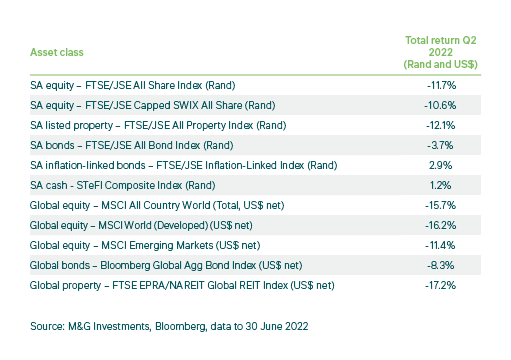

Investor concerns over a major slowdown in global growth, and therefore corporate earnings, escalated during the second quarter (Q2) of 2022, especially in June. This came as steep interest rate hikes in the US and strict Chinese Covid-19 lockdowns, as well as the ongoing destructive Russia-Ukraine war, led to downward revisions in economic growth expectations for the world’s biggest economies. Further rises in energy and food prices also led to more speculation over extended inflationary pressures and stagflation and/or recession, even as other commodity prices lost ground. This combination of factors resulted in losses across most financial markets – equities, nominal bonds and inflation-linked bonds. For the quarter ended 30 June 2022, the MSCI All Country World Index returned -15.7%, the MSCI Emerging Markets Index produced -11.4%, and the Bloomberg Global Aggregate Bond Index delivered -8.3% (all in US$).

South African markets were less insulated from the global inflation and growth concerns than in the previous quarter. This was due to the fall in commodity prices, accelerating inflation, and forecasts for more aggressive local interest rate hikes in July, plus even slower growth ahead. Stage 4-6 loadshedding also weighed on growth prospects. However, local bond and equity losses were somewhat less severe than developed markets, and more in line with those in other emerging markets. The FTSE/JSE All Share Index (ALSI) returned -11.7% for the quarter and the Capped SWIX -10.6%, dragged down by Resources with a -21.9% return, -15.8% from Financials, -12.1% from Listed Property (All Property Index) and -3.0% from Industrials. For the six months of 2022 so far, the ALSI has returned -8.3%, outperforming the -18.2% recorded by global equities (the MSCI All Country World Index), both in rand terms.

Amid growing inflationary fears, SA’s All Bond Index lost 3.7%, but inflation-linked bonds (ILBs) delivered 2.9% and cash returned 1.2%. Finally, the rand weakened significantly against the US dollar and other major global currencies during Q2, losing 12.1% versus the greenback, 3.4% versus the UK pound sterling and 5.4% against the euro. This depreciation would have bolstered SA investors’ foreign-currency returns.

In the US, inflation hit 8.6% y/y in May, the highest since 1981 and above market forecasts of 8.3% y/y. At the same time, US economic growth shrank by 1.6% y/y in Q1 2022 as consumer incomes and corporate profits were hit by higher prices for food and energy and the end of Covid-related stimulus payments. The US Federal Reserve’s 75bp rate hike in June was an aggressive response to this accelerating inflation, a move which prompted more market-watchers to predict a recession ahead. Many noted that, given that inflation has largely stemmed from supply-side factors, higher interest rates were not likely to be as effective in curbing inflation as with demand-driven factors. Fed policymakers now see rates reaching 3.4% in 2022, well above the 1.9% forecast in March, as well as increased chances of recession.

US Treasury bonds sold off sharply as a consequence of the deteriorating inflation and interest rate outlook, resulting in an unusually volatile market: the Bloomberg Aggregate US Treasuries Index returned -9.2% in US$, after the -6.2% recorded in Q1. Meanwhile, US equity markets were deeply in the red for the quarter: in US dollars, the Nasdaq delivered – 22.3%, the Dow Jones produced -10.8% and the S&P 500 returned -16.1%. The S&P 500, the broadest benchmark for the US equity market, produced its worst performance for the first six months of any year since 1970, down 20.0%.

In the UK, the Bank of England implemented another interest rate hike in June, taking its main bank rate to 1.25%, the highest level in 13 years. This came against inflation of 9.1% y/y in May. However, the central bank remained less aggressive on its outlook for rate hikes compared to the Federal Reserve. For Q2 2022, UK equities were also deeply in the red: the FTSE 100 returned -11.2% in US dollars.

Meanwhile, the European Central Bank (ECB) largely stuck to its Q1 plans, saying it would accelerate the winding down of its bond purchases from July, and signalling an upcoming 25bp rate hike. This was largely in line with market expectations. The Bank also revised its economic growth outlook lower to 2.8% for 2022 (from 3.7%) and 2.1% for 2023 (from 2.8%). Despite an acceleration in Q1 GDP growth to 5.4% y/y in the Eurozone, market watchers are more worried about a coming recession in the region due to its less-flexible economic structure; it continues to recover more slowly from the Coronavirus crisis than the US and UK. In France, the CAC 40 returned -14.4%, while Germany’s DAX delivered -16.7% for the quarter in US dollars.

In Japan, the Bank of Japan (BOJ) continued to be the only major central bank to maintain an ultra-easy monetary policy during the quarter, as it left its policy rate unchanged at -0.1%. The market continues to forecast no interest rate hikes through 2023. Japan’s Q1 2022 GDP growth was reported at -0.5%, slower than the 1.0% expected, and the equity market also lost ground with the Nikkei returning -15.1% in US dollars for the quarter.

Chinese investors became more upbeat towards the end of the quarter as Covid infection rates started to slow, allowing the government to ease some of its ultra-strict lockdown conditions in Shanghai and certain other areas. The country recorded better-than-expected GDP growth of 4.8% y/y in Q1, up from 4.0% y/y the previous quarter, and the latest data showed a surge in manufacturing and non-manufacturing PMI in June, accelerating to 51.7 (up from 48.1) and 54.7 (up from 47.8) respectively. The People’s Bank of China (PBOC) left interest rates unchanged at its June meeting, in line with expectations. The central bank is concerned not only about growth, but also about the widening divergence between local and US interest rates, which has put Chinese bonds and the yuan under selling pressure. For the quarter, Hong Kong’s Hang Seng produced 0.7%, while the MSCI China returned 3.5%, both in US dollars.

Other large emerging equity markets were in the red for the quarter, all in US$ terms, with Brazil’s Bovespa the worst performer at -25.4%. The MSCI South Africa was close behind with -22.9%, while South Korea’s KOSPI was down 20.8%, the MSCI India fell 13.5% and the MSCI Turkey recorded a -10.9% return.

Energy prices continued their rise, but at a moderated pace: Brent crude oil gained 6.4% during the quarter after experiencing some softness in June. Year-to-date the price is up some 47% in US dollars. Looking at precious metals, gold fell 6.0% for the quarter, while platinum lost 7.7% and palladium was down 13.2%. Other industrial metals prices lost between 20-30% amid heightened worries of a global growth slowdown.

South Africa

South Africa’s fragile economic recovery came under increasing pressure in Q2: growth prospects took a downturn due to the renewal of national Stage 4-6 loadshedding, severe flooding in KwaZulu Natal, rising inflation and higher-than-expected interest rate hikes, as well as the retreat in commodity prices. The South African Reserve Bank (SARB) lowered its GDP growth forecast for 2022 to 1.7% from 2.0% previously.

With CPI rising to 6.5% y/y in May – the first time since January 2017 that it has broken through the upper limit of the SARB’s 3%-6% target range – the SARB hiked the repo rate by 50bps at its May meeting to 4.75%. The Bank is widely expected to hike by another 100bps at a minimum this year in an effort to both fight inflation and to keep our interest rate differential versus the US as high as possible in a bid to avoid more pressure on the rand and SA bond yields.

How have our views and portfolio positioning changed in Q2 2022?

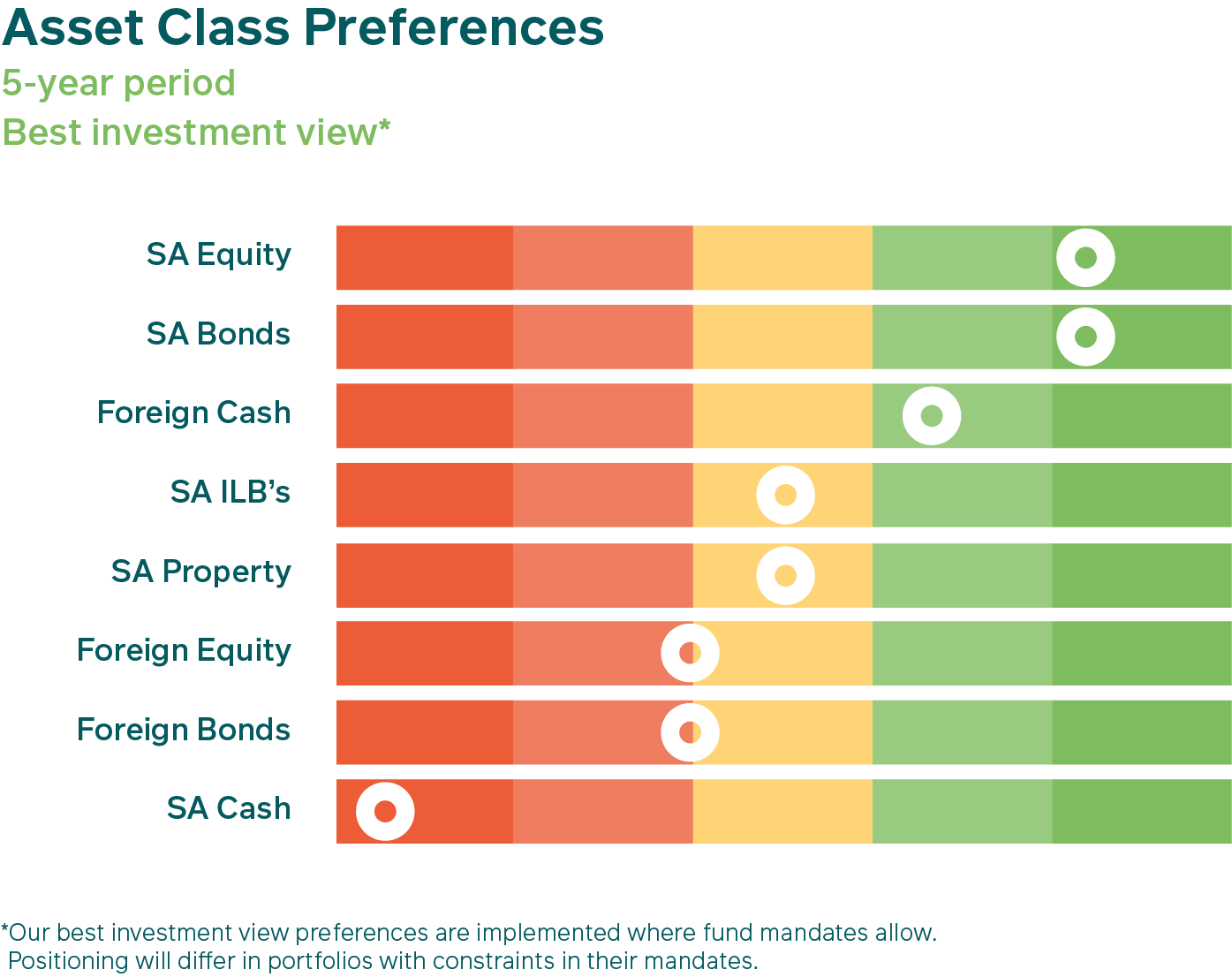

Starting with our view on offshore asset allocation, we maintained our portfolio positioning favouring local assets over global assets, which proved to be somewhat supportive for portfolio returns due to the relative outperformance of SA assets versus their global counterparts.

Within our global holdings, we continued to prefer global cash over both global equities and bonds in order to keep risk relatively low, while also being able to take advantage of market mis-pricing episodes that might arise. This positioning turned out to be favourable for our portfolios on a relative basis for the quarter, based on the weakness in both global equity and bond markets compared to global cash. Within our global equity positioning, we kept our active weight the same through the quarter, thus any changes in the total weight of equities reflect the drift due to market falls. Our exposure to a broad mix of equity markets with diversified return profiles has helped to partly cushion our funds against the current market downturn.

Within global bonds, we took advantage of the sharp selloff and reduced our underweight in developed market bonds, adding some US Treasury and diversified global bond exposure. We are still underweight global bonds and have a preference for bond markets where the real yields are high and the currency is trading at fair-to-cheap levels. We maintained our underweight stance on investment-grade corporate credit, holding almost no exposure despite improving valuations over the quarter as spreads widened. We continued to believe that corporate yield spreads are not sufficiently high for the risk involved.

Our best investment view portfolios like the M&G Balanced Fund still favoured SA equities at the end of Q2. During the quarter we made very few adjustments in our holdings, and none with a meaningful impact. Given the large price declines across most locally listed shares during the period, SA equity valuations (as measured by the 12-month forward Price/Earnings ratio of the FTSE/JSE Capped SWIX Index) de-rated over the quarter, falling from around 9.6X at the beginning of the quarter to around 8.0X at quarter-end. Corporate earnings expectations have started to roll over, but not by as much as share price losses, and are yet to reflect global recession risks.

Within SA equities, among the main holdings contributing to our House View portfolios’ performance during the quarter were Naspers and Prosus, given their sharp share price rebounds in June on the back of their announcement of a new open-ended share-repurchase programme financed by Prosus’ sale of Tencent shares. Along with other investors we welcomed this move, as the company signalled its willingness to exploit the valuation discounts the market has placed on its underlying assets. Other meaningful contributions came from our overweights in British American Tobacco, a traditionally defensive company that again proved its value, as well as Sasol.

Among our portfolio’s largest detractors for the quarter were our active Resources and Financial holdings, as well as MTN and Foschini, against the backdrop of non-energy commodity price weakness and downgrades to economic growth expectations. As a reminder, in the previous quarter we trimmed our Retail sector exposure due to the deteriorating inflation and interest rate outlook, which now present even more significant headwinds for retail sales.

We maintained our neutral positioning in SA listed property in Q2 2022, preferring to hold other shares that we consider offer better value propositions for less risk. Conditions in the local property sector remain uncertain given the rising local interest rate cycle (many property companies are reliant on finance to expand their portfolios) and relatively weak growth prospects, among other fundamental factors.

On a relative basis, our portfolios benefitted from our ongoing preference for SA nominal bonds in the second quarter thanks to their outperformance of SA equities, as well as global equities and global bonds. We did add modestly to our portfolios’ nominal bond exposure out of SA cash holdings during the quarter amid market weakness, increasing our overweight position in this asset class. We still believe nominal bonds remain attractive relative to both other income assets and their own longer-term history, and will more than compensate investors for their associated risks.

Although we are not holding inflation-linked bonds (ILBs) in our House View portfolios to a meaningful degree, we do hold them in our real return portfolios like the M&G Inflation Plus Fund, where we currently have a neutral view. We still believe that ILB real yields remain relatively attractive compared to their own history and our long-run fair value assumption, but compared to nominal bonds, their valuations are less attractive and they have lower return potential.

Lastly, despite the SARB’s interest rate hikes during the quarter, our House View portfolios remained tilted away from SA cash as our least-preferred asset class, given the extremely low base rate off which the SARB has hiked. During the quarter we reduced our cash exposure in order to add more SA nominal bonds to the portfolios to take advantage of the even more attractive valuations on offer. In our view, other SA assets remain more attractive on a relative basis.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter