South Africa

South Africa Namibia

Namibia

M&G Investments

M&G Investments

Five ways to avoid running out of retirement money

Various studies have shown that the vast majority of retirement fund members won’t have sufficient capital to sustain their standard of living in retirement. For many, this realisation often comes too late, at a time in their lives when there is very little that they can do to correct past mistakes. Retirees who find themselves in this position often end up having to either significantly reduce the income that they draw, liquidate their larger assets (e.g. downscaling their home), or move in with family members.

Fortunately, for those who are still in their pre-retirement years, it’s not too late. There are at least five things they can do or levers they can adjust to increase the probability of retiring comfortably and also lower their risk of running out of money. In this article we briefly explain each option or planning parameter, with a particular focus on investment returns.

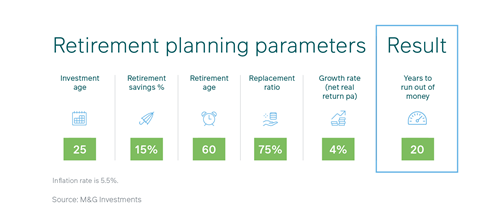

1. Investment age is the first parameter when it comes to planning, and is very important, since the earlier you start the more time you will have both to invest and for your investments to grow. There are various ways to adjust the other parameters on your retirement journey, but if you start late there’s no going back. In the example above, starting to invest at age 25 and following these other parameters diligently will yield this result.

2. Retirement savings percentage refers to the average percentage of your salary you contribute to your retirement savings throughout the time you are investing. The effort of consistently sticking with a 15% contribution every month will help you reach your retirement goals more easily. Of course, this 15% can be increased to improve your outcomes – and should be if you can afford it. For example, if you lift it to 18% in the example above, your years of income in retirement increase by an additional 10 years – an entire decade!

3. Retirement age refers to the average age of retirement. In South Africa, this is 60 years old, but there can be opportunities to work longer. If you are behind on your savings and are able to work longer, it’s often the best option as you will have more time to add to your retirement fund (and less time to withdraw from your pension-providing vehicle).

4. Replacement ratio is the percentage of your final salary that you hope to draw per month as a regular income in retirement. The 75% replacement ratio is the average ratio that retirement planning strives for – an industry standard. It assumes that major debt such as your home and car will be paid off at retirement and some of your living expenses will be reduced, even though your medical expenses are likely to increase. While 75% is the minimum goal, it has been harder and harder to achieve this in recent years. By lowering your replacement ratio, you will have to live on a lower income, but this option will also reduce the amount of time it takes to deplete your savings, while allowing more of your remaining capital to grow over time.

You can use our Retirement Calculator to assess your savings progress so far and what changes you might need to make to reach your desired income.

5. Growth rate (net real return per annum) refers to the rate of return that your investment would need to earn to reach your goal of investing enough, taking inflation into account. The example above is factoring in a return of 4% above inflation, which is relatively conservative as the average return you could expect from a multi-asset low-equity portfolio over time. SA equities, meanwhile, have historically delivered 7% above inflation on average. So opting to keep a higher-than-average exposure to equities in your portfolio over time, where you could earn an average of 6% above inflation, for example, is another key way to increase the years you’d have before running out of money. With people living into their 90s these days, the prospect of staying invested for 30 years past retirement is certainly a long enough time frame to reduce the risk of holding more equities. However, keep in mind that while building up your retirement savings you will need to comply with Regulation 28 of the Pension Funds Act, which limits the amount of exposure your retirement portfolio can have to equities to a maximum of 75%.

Years until you run out of money is the final result of the other factors above. This is how long your retirement will be funded -- and in the above example, 20 years could be too short. Three decades, as mentioned above, would be a more appropriate timeframe to aim for.

In conclusion, a financial adviser is well-positioned to assist in working out how to choose your parameters – and how they should change during your pre-retirement saving years as well as post-retirement. Being overly cautious of investment risk or volatility, especially once you retire and need to keep investing your accumulated retirement savings, is a common misstep to be aware of. Investment exposure to volatile assets can be an important component of living the retirement you dream of.

For more information or to invest with M&G Investments, please visit www.mandg.co.za or feel free to contact our Client Services Team 0860 105 775 or email us at info@mandg.co.za.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter