South Africa

South Africa Namibia

Namibia

Gareth Bern

CIO Fixed Income

COMMENT ON: Credit rating downgrade and SA government bonds

The last few weeks have seen a significant sell-off in SA government bond yields. The repricing has been notable, not just by the sheer scale of the sell-off but also for its speed. Both are at extremes. During the course of March, bond yields had sold off over 3% at one point. Intra-day volatility in the bond market has likewise been seen on an almost unprecedented scale. Figure 1 reflects the yield on a generic 20-year bond over the last 20 years, as well as the prospective real yield on offer.

FIGURE ONE

On almost any valuation metric, SA government bonds look cheap. The fact is, we felt this was already the case in February before the sell-off and had written about this at the time.

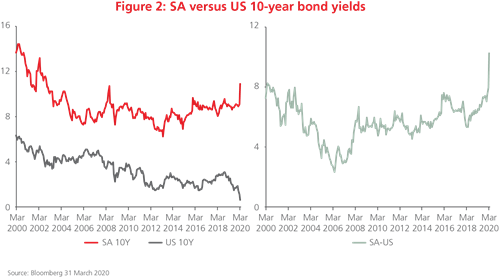

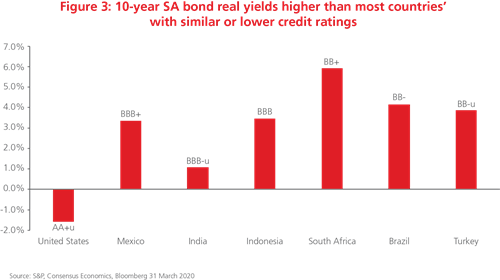

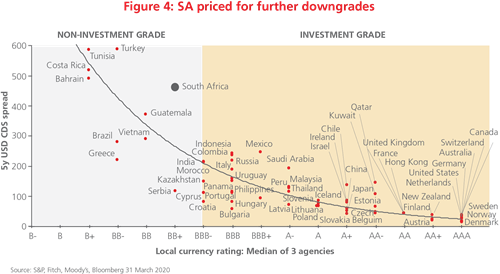

The reality is that today we are orders of magnitude cheaper than February. We have highlighted a few of these measures below. Whichever metric one wants to use the answer is the same to us – SA government bonds appear to offer significant value and are pricing in a substantial risk premium. Their spread above US Treasuries is far higher than during the Global Financial Crisis (GFC), as shown in Figure 2; their real yields are higher than other emerging markets with even worse credit ratings (Figure 3); and their yields are still reflecting the likelihood of further credit rating downgrades to come following that by Moody’s on 27 March (Figure 4).

FIGURE TWO

FIGURE THREE

FIGURE FOUR

Some context

The catalyst for the repricing has been the COVID-19 pandemic and its economic impact not just locally but globally. We have seen a global sell-off of all risk assets, with the local equity, property, and bond markets suffering massive falls in value. The impact of the fall in asset prices, as well as the speed of the repricing, appear to have impacted on liquidity in the local bond market which only sought to further compound and accelerate the sell-off in local bonds.

Later we saw the South African Reserve Bank (SARB) look to address the lack of liquidity in the bond market by introducing several supportive measures. One was the announcement that they would buy SA government bonds to provide liquidity. Bond yields rallied on this announcement and we feel the move does provide some form of ‘floor’ as to how much more bond yields can fall – as it is likely (in our opinion) the SARB will intervene if similar stresses arise in the bond market.

Fiscal concerns

What we have grappled with is the fiscal impact of the virus on South Africa. It certainly has and will impact growth – the quantum, however, is unknown. South Africa’s fiscal position was stretched before any impact from the virus – any fiscal response to the virus will be against this backdrop versus, for instance, the more sound fiscal position the country found itself in before the GFC. More government spending necessarily means more bond issuance. Plus, the cost of any fiscal response will be higher due to the rising cost of SA government debt as evidenced by bond yields. Contrast that to developed countries who can borrow at close to a zero interest rate.

But what about the downgrade?

As we have discussed previously, our view has been that SA bonds had been priced for a downgrade for some time. It would be difficult to argue that the Moody’s downgrade was a surprise to anyone. One unknown is the number of forced sellers of SA bonds there might be, as SA will leave the investment-grade bond index and enter the high-yield indices. Estimates have varied significantly – in our view, there probably will be some selling, but it is also not improbable that it turns out to be less than expected. It has also been announced that the re-weighting of the indices will be delayed due to COVID-19 so the actual exit from the index is somewhat delayed. Bond yields have in fact rallied post the downgrade.

What have we done?

The fiscal concerns caused us to be more cautious as bonds sold off during the first weeks of March, which turned out to be the right decision. As we often highlight, we have no crystal ball as to where local bond yields may go in the short term and what that path might look like.

What we do know is that on almost any measure, SA government bonds appear cheap; although that is against an uncertain backdrop of an unknown impact of an impending domestic and global health crisis. We do know that SA government bonds have seen a massive sell-off – whether this is warranted or not is an open question. We also know that investors are being offered significant compensation versus the case just a few weeks ago for these risks.

Against this backdrop, we have felt it appropriate to take advantage of these moves and as such added to our government bond positions across our various fixed income funds. While investors are likely to experience more volatility in the months ahead, valuations are in our favour, and on a medium- to long-term basis we feel investors should be well rewarded.

For more information or if you have any questions, please feel free to call our Client Services Team on 0860 105 775 or email us at query@prudential.co.za.

Share

Did you enjoy this article?

Get the Newsletter

Get the Newsletter